Daily Market Update: 25 July, 2025

The key takeaways from the last 24 hours

Millionaire factory mauled

S&P/ASX 200 Index (ASX: XJO) closed 27.8 points, or 0.3 per cent, weaker at 8709.4 on Thursday, with nine of the 11 sectors losing ground, led by energy, industrials and real estate stocks. The broader All Ordinaries Index (ASX: XAO) gave up 22 points, or 0.2 per cent, to 8,979.4.

Macquarie Group Limited (ASX: MQG) slumped $11.45, or 5.1 per cent, to $213.84 after the asset management and investment banking firm was hit with its first-ever protest vote on its remuneration report at its annual general meeting, following regulatory and compliance failings. A similar vote next year could lead to a board spill. The group also announced that its long-serving chief financial officer Alex Harvey would depart. Three of the big four banks closed higher. National Australia Bank Limited (ASX: NAB) pushed 46 cents, or 1.2 per cent, higher to $37.66; Westpac Banking Corporation (ASX: WBC) rose 18 cents, or 0.5 per cent, to $33.29; and Commonwealth Bank of Australia (ASX: CBA) edged ahead by 17 cents, or 0.1 per cent, to $173.47; but Australia and New Zealand Banking Group Limited (ASX: ANZ)weakened 13 cents, or 0.4 per cent, to $30.44.

Elsewhere in industrials (which fell 1.2 per cent) Computershare Limited (ASX: CPU) fell $1.37, or 3.3 per cent, to $40.22; Brambles Limited (ASX: BXB) retreated 36 cents, or 1.5 per cent, to $23.13; Cleanaway Waste Management Limited (ASX: CWY) shed 5 cents, or 1.7 per cent, to $2.85; and rail group Aurizon Holdings Limited (ASX: AZJ) lost 7 cents, or 2.1 per cent, to $3.26. Biotech heavyweight CSL Limited (ASX: CSL) gained $4.06, or 1.5 per cent, to $269.56. Automotive parts group Bapcor Limited (ASX: BAP) had a shocker, tanking $1.45, or 28.4 per cent, to $3.66 after it warned of weaker-than-expected earnings; announced $50 million in post-tax write-downs; and said three directors would leave the board.

Lynas, Fortescue flying

In big mining, BHP Group Limited (ASX: BHP) leaked 25 cents, or 0.6 per cent, to $41.60; Rio Tinto Limited (ASX: RIO) advanced 39 cents, or 0.3 per cent, to $119.86; and Fortescue Metals Group Limited (ASX: FMG) climbed 79 cents, or 4.3 per cent, to $19.00. Fortescue Metals Group Limited (ASX: FMG) told the market that it shipped a record amount of iron ore in the year to June and is forecasting further volume growth in the next 12 months at a lower cost of production. But the company flagged a $227 million impairment on two failed energy projects, confirming that its Arizona hydrogen and Gladstone electrolyser projects would not go ahead. Rare earths producer Lynas Rare Earths Limited (ASX: LYC) surged 51 cents, or 5 per cent, to $10.65, after breaking its production record by producing 2,080 tonnes of neodymium-praseodymium (NdPr) in the most recent quarter, up 38 per cent on the previous quarter’s output. Total rare earth oxide (REO) production rose 68 per cent to 3,212 tonnes, and Lynas notched its best average selling price for three years, at US$60.20 per kilogram. Sales revenue rose by 38 per cent on the previous quarter, to $170.2 million. Lynas also signed a memorandum of understanding with Korean permanent magnet manufacturer JS Link for a potential manufacturing and supply partnership.

Gold miners were under pressure as the precious metal’s price retreated, on easing global tensions. Evolution Mining Limited (ASX: EVN) slid 21 cents, or 2.7 per cent, to $7.54; Regis Resources Limited (ASX: RRL) walked back 10 cents, or 2.2 per cent, to $4.36; and Northern Star Resources Limited (ASX: NST) gave up 40 cents, or 2.4 per cent, to $16.27, after saying it had ditched its forward hedging policy, so as to take advantage of the soaring gold spot price, while acknowledging that troubles at its Super Pit mine in Kalgoorlie would continue to limit production. In coal, Whitehaven Coal Limited (ASX: WHC) surrendered 15 cents, or 2.1 per cent, to $7.03; and New Hope Corporation Limited (ASX: NHC) eased 2 cents, or 0.5 per cent, to $4.36.

Fresh record closes for S&P 500, Nasdaq

In the US, the broad Standard & Poor’s 500 Index (NYSEARCA: SPY) and the tech-laden Nasdaq Composite Index (NASDAQ: IXIC) both moved to record closes overnight after Alphabet Inc. (NASDAQ: GOOGL)’s latest quarterly results came in better than expected. The S&P 500 added a minuscule 4.4 points, or 0.1 per cent if rounded-up, to end at 6,363.35, but it was enough for a record close after a new intraday all-time high earlier in the session. The Nasdaq Composite Index (NASDAQ: IXIC) pulled off the same feat, rising 37.94 points, or 0.2 per cent, to close at 21,057.96. But the blue-chip 30-stock Dow Jones Industrial Average (INDEXDJX: DJI) slid 316.38 points, or 0.7 per cent, to settle at 44,693.91, bogged down by a 7 per cent plunge in International Business Machines Corporation (NYSE: IBM) after its second-quarter software revenue missed expectations.

The S&P 500 was helped by a strong quarterly earnings report from Alphabet Inc. (NASDAQ: GOOGL), which reported a 32 per cent jump in Google Cloud revenue to US$13.6 billion, well ahead of the US$13.1 billion consensus forecast from analysts. Investors are also nervously eyeing the visit tonight by President Trump to the Federal Reserve, for, presumably, discussions with Chairman Powell. It will be the first time in nearly two decades that an American President will make an official trip to the central bank – and it is probably not going to be a social chat over scones and tea.

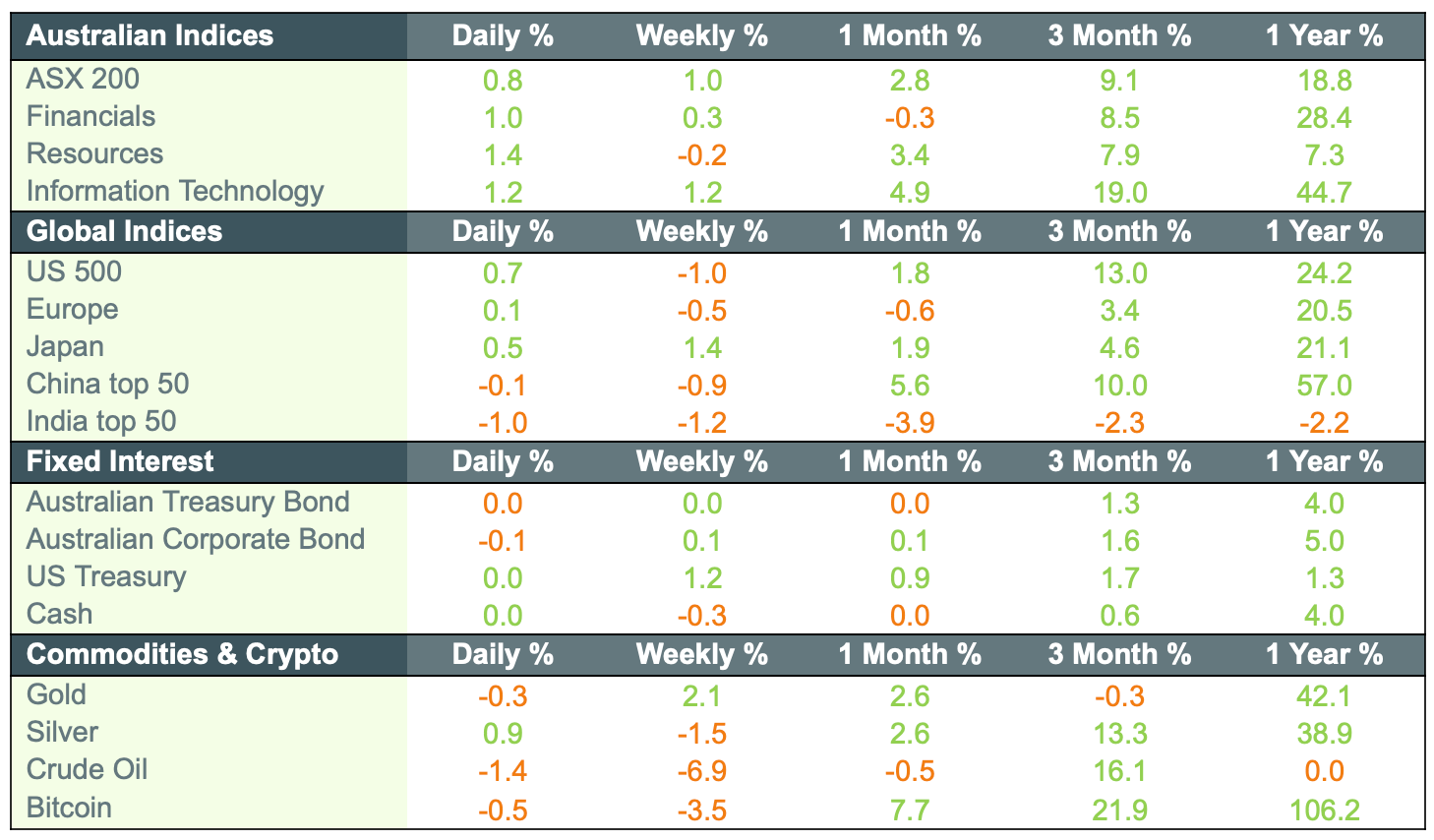

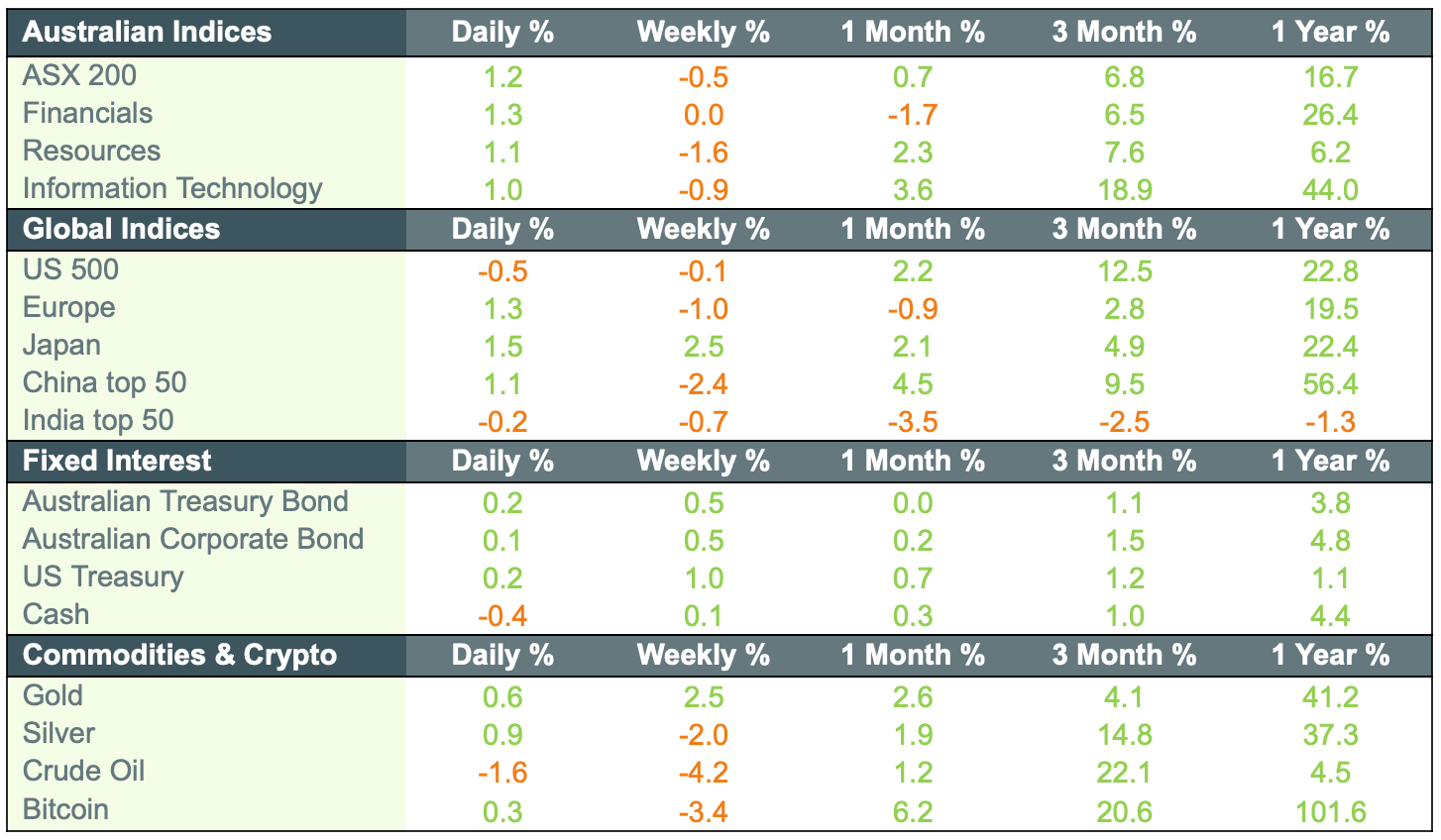

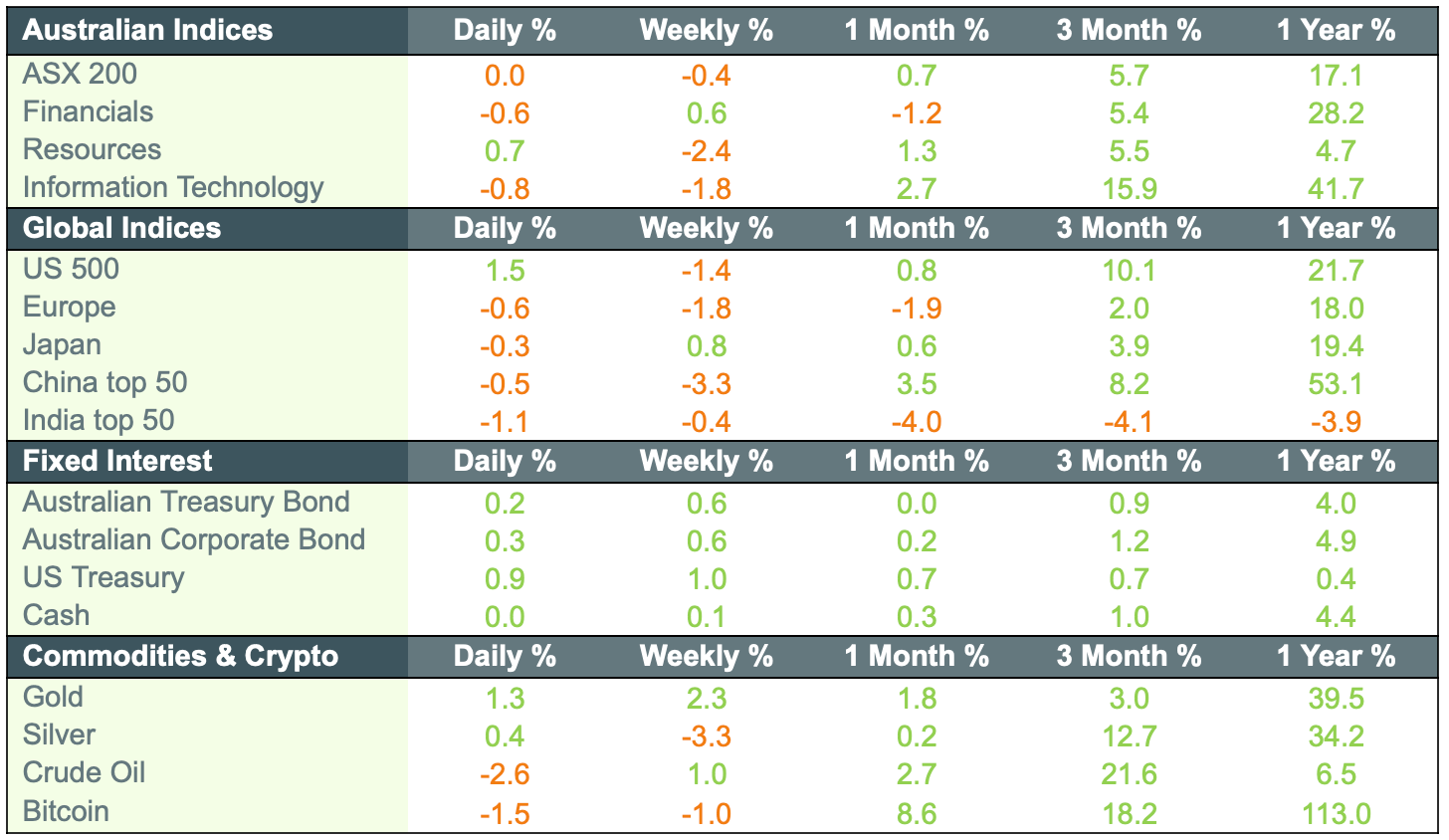

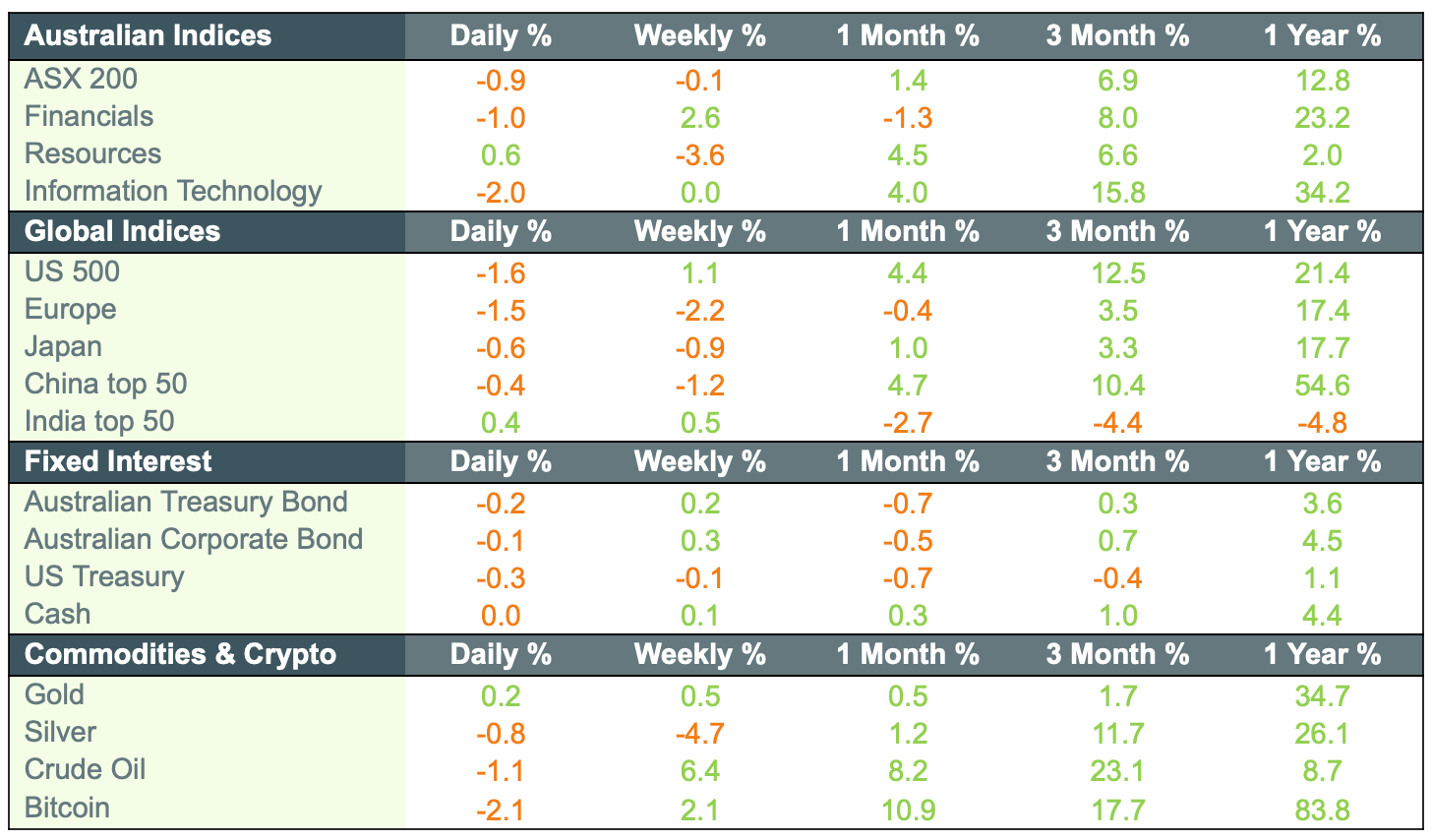

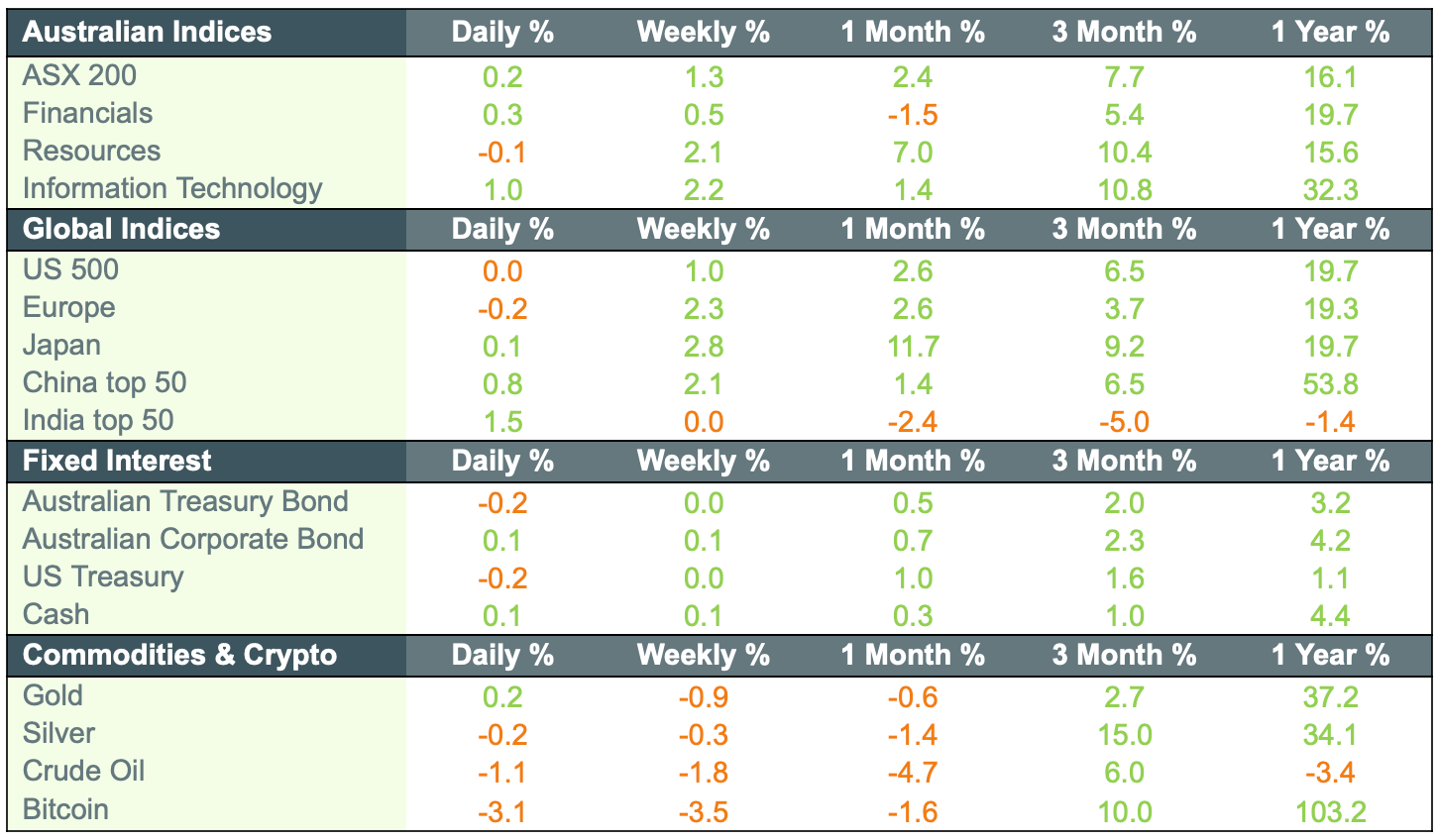

Market movements