Daily Market Update: 14 July, 2025

The key takeaways from the last 24 hours

ASX closes lower despite iron ore rebound; BHP and Rio Tinto extend gains, Johns Lyng jumps on takeover

The local market briefly broke through the 8,600 point level on Friday, only to finish 9 points lower, as the S&P/ASX 200 Index (ASX: XJO) closed down 0.1 per cent. The weakness was due to another barrage of tariff announcements from Trump: a plan to levy every trading partner a tariff of 15 to 20 per cent, and 35 per cent on Canadian imports. The result was a 0.3 per cent decline for the week. The materials sector was the standout as Rio Tinto Limited (ASX: RIO) gained 2.3 per cent and BHP Group Limited (ASX: BHP) 2.8 per cent, as Chinese stimulus hopes grow. BHP has climbed more than 10 per cent in the last three weeks, and Fortescue Metals Group Limited (ASX: FMG) an impressive 17 per cent. Engineering group Johns Lyng Group Limited (ASX: JLG) was the ultimate standout as the company agreed to a $1.3 billion deal that will see it sold to Pacific Equity Partners for $3.90 per share, with the stock up 22 per cent on the news. Ventia Services Group Limited (ASX: VNT) fell close to 2 per cent despite the company increasing the scope of its agreement with the NBN by nearly $300 million.

Markets stall on tariff talk, but historical trends signal upside; Tesla expands to India, Ferrero makes $3.1 billion play

The Dow Jones Industrial Average (INDEXDJX: DJI) fell 0.6 per cent, while the S&P 500 Index (NYSE: SPX) slipped 0.3 per cent from an all-time high as tariff rhetoric intensified once again. A rally that saw five record highs in nine trading days showed signs of reversing amid the threat of a 35 per cent tariff on key Canadian imports. Kraft Heinz Company (NASDAQ: KHC), known for its ketchup, rose more than 2 per cent as management flagged plans to sell off parts of the slowing global business, while Bitcoin hit another all-time high as index and ETF providers continue to enter the market. Five of the Magnificent Seven gained, including Tesla Inc (NASDAQ: TSLA), which climbed more than 1 per cent after the company confirmed the opening of its first Indian store and the intention to start deliveries sooner rather than later. According to analysis, any time the S&P 500 Index (NYSE: SPX) increases more than 20 per cent in two months or less, it has been consistently higher 12 months later, and by an average of 15 per cent. Ferrero International, the Italian food brand, has shocked the market in a deal to buy US giant WK Kellogg for USD 3.1 billion, a premium of 31 per cent to the closing price.

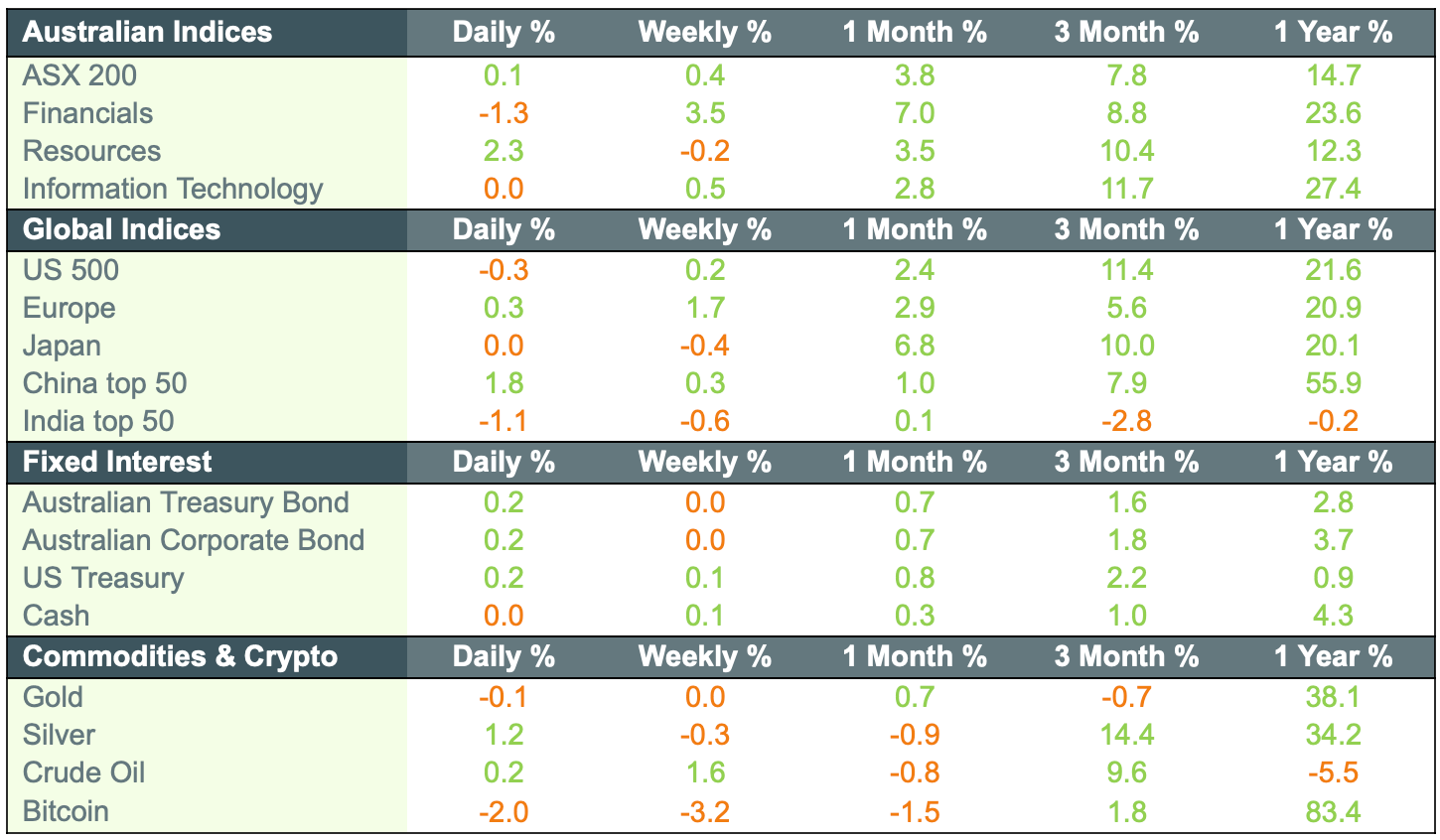

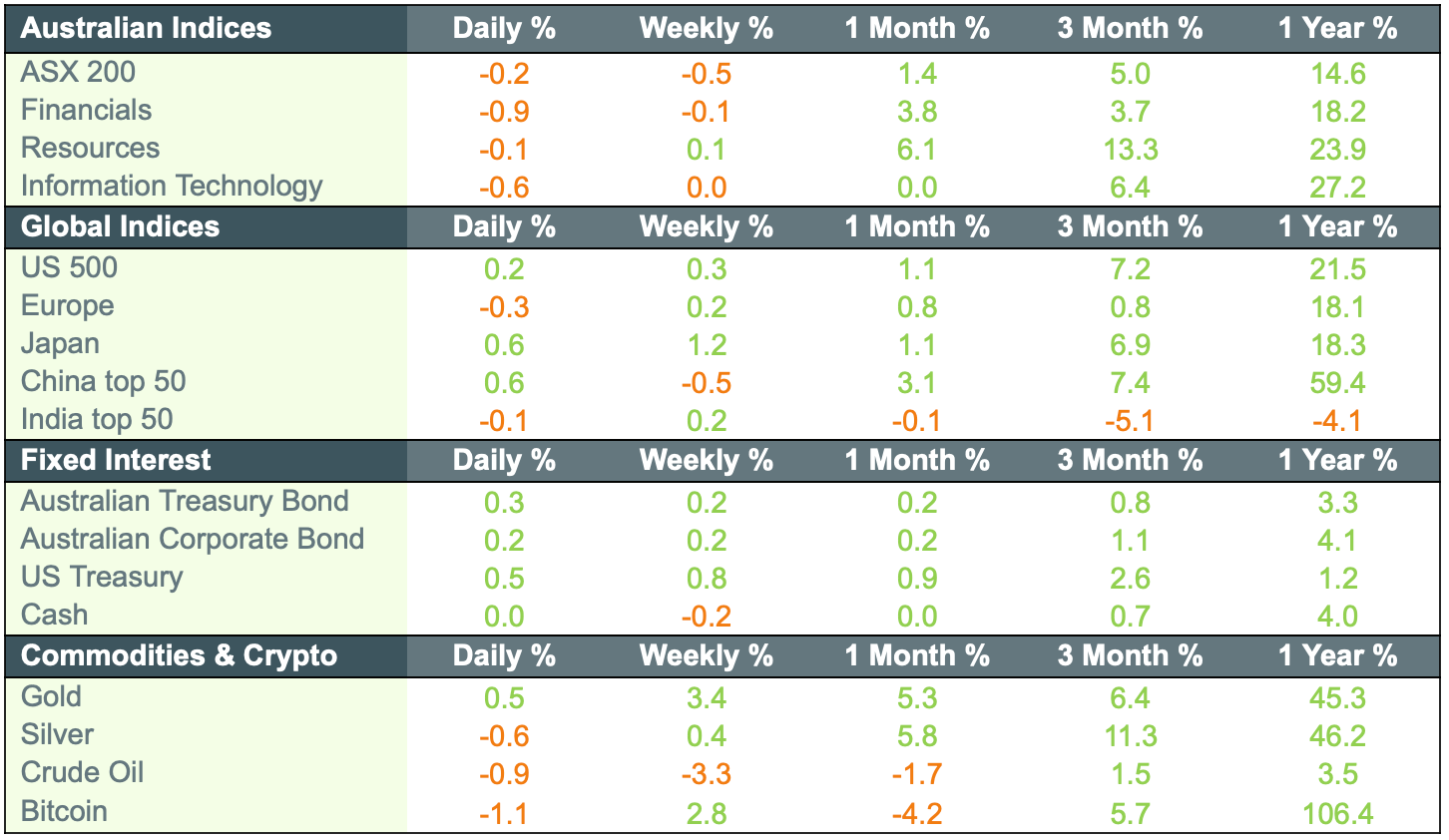

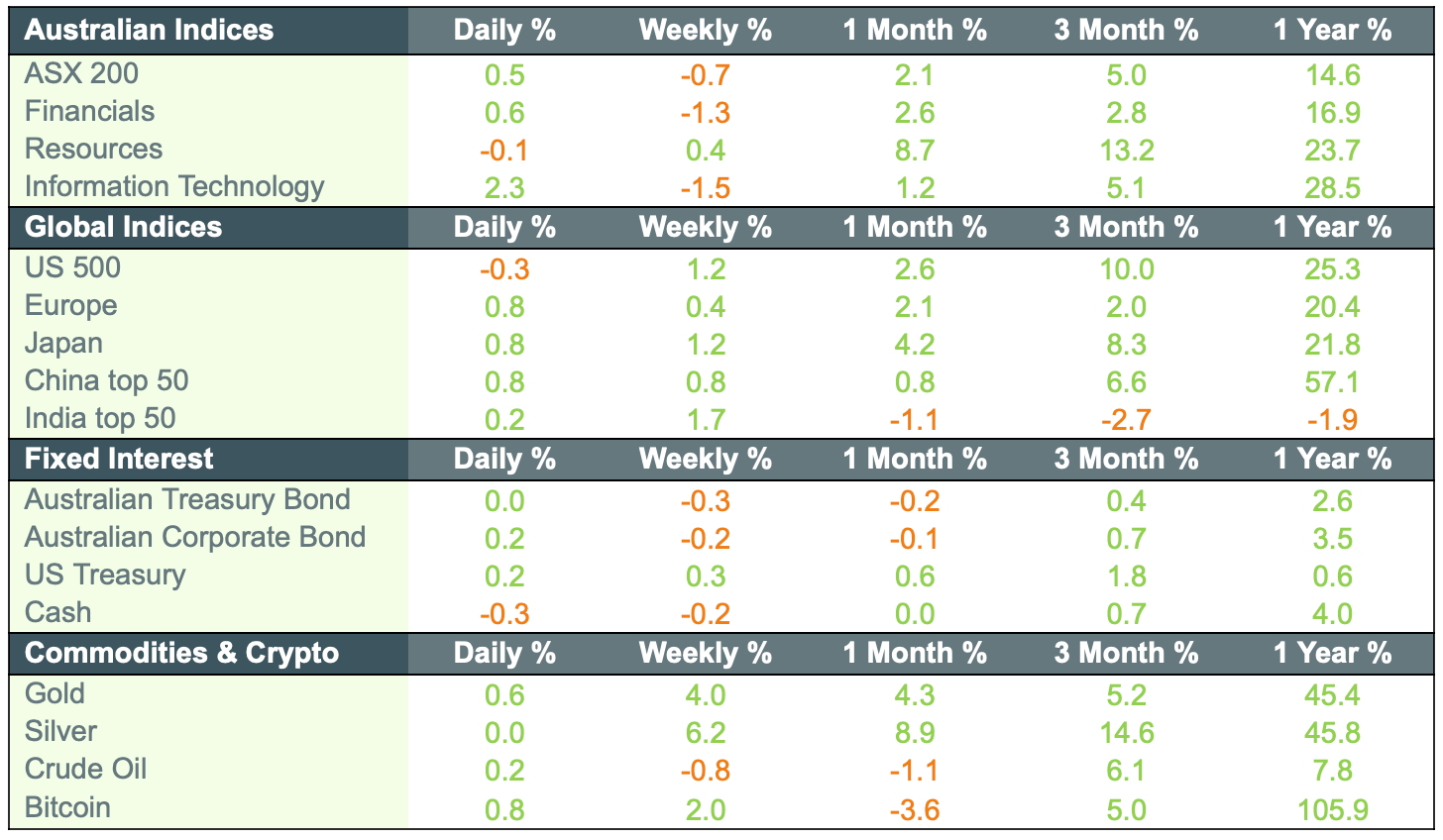

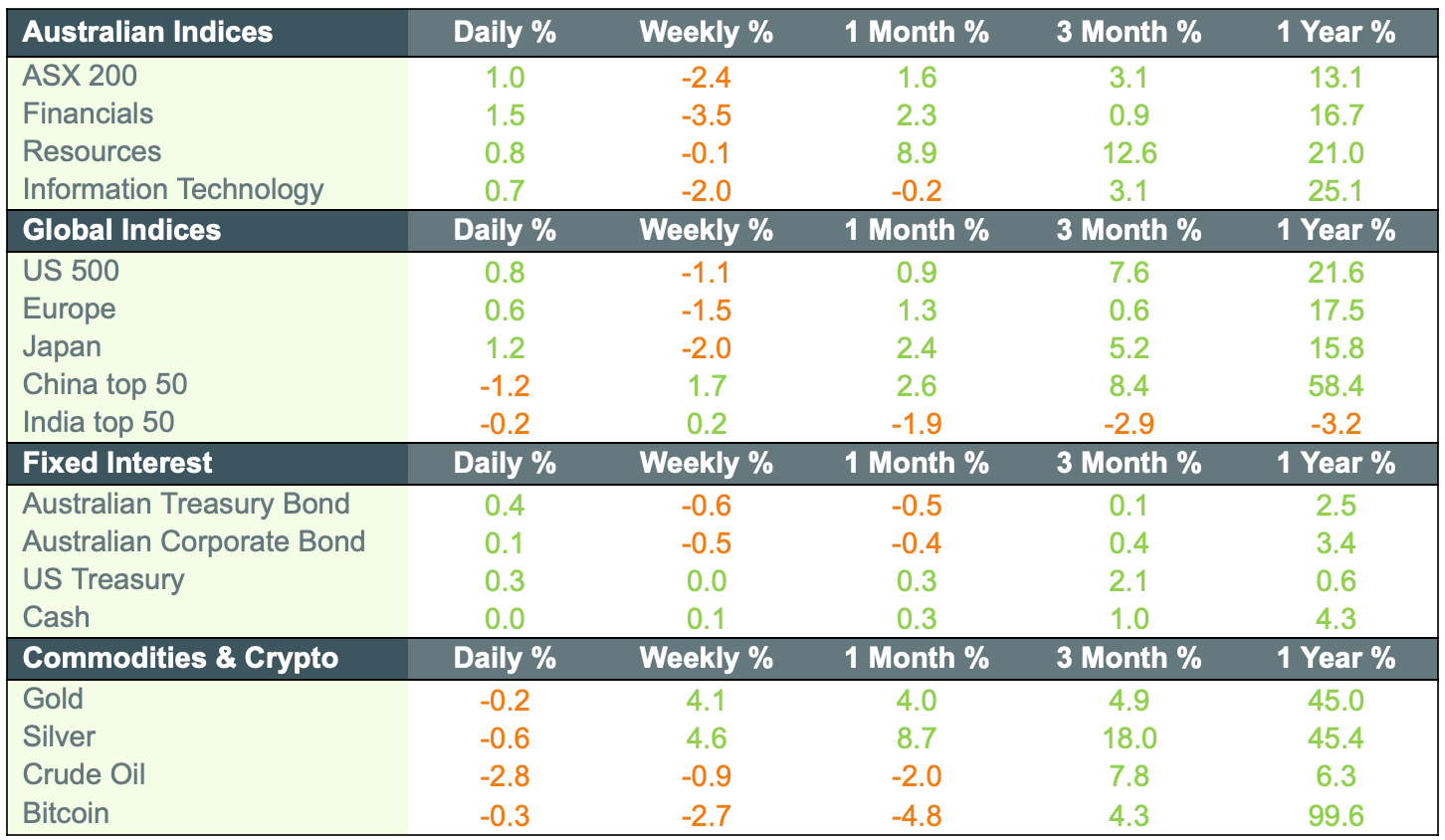

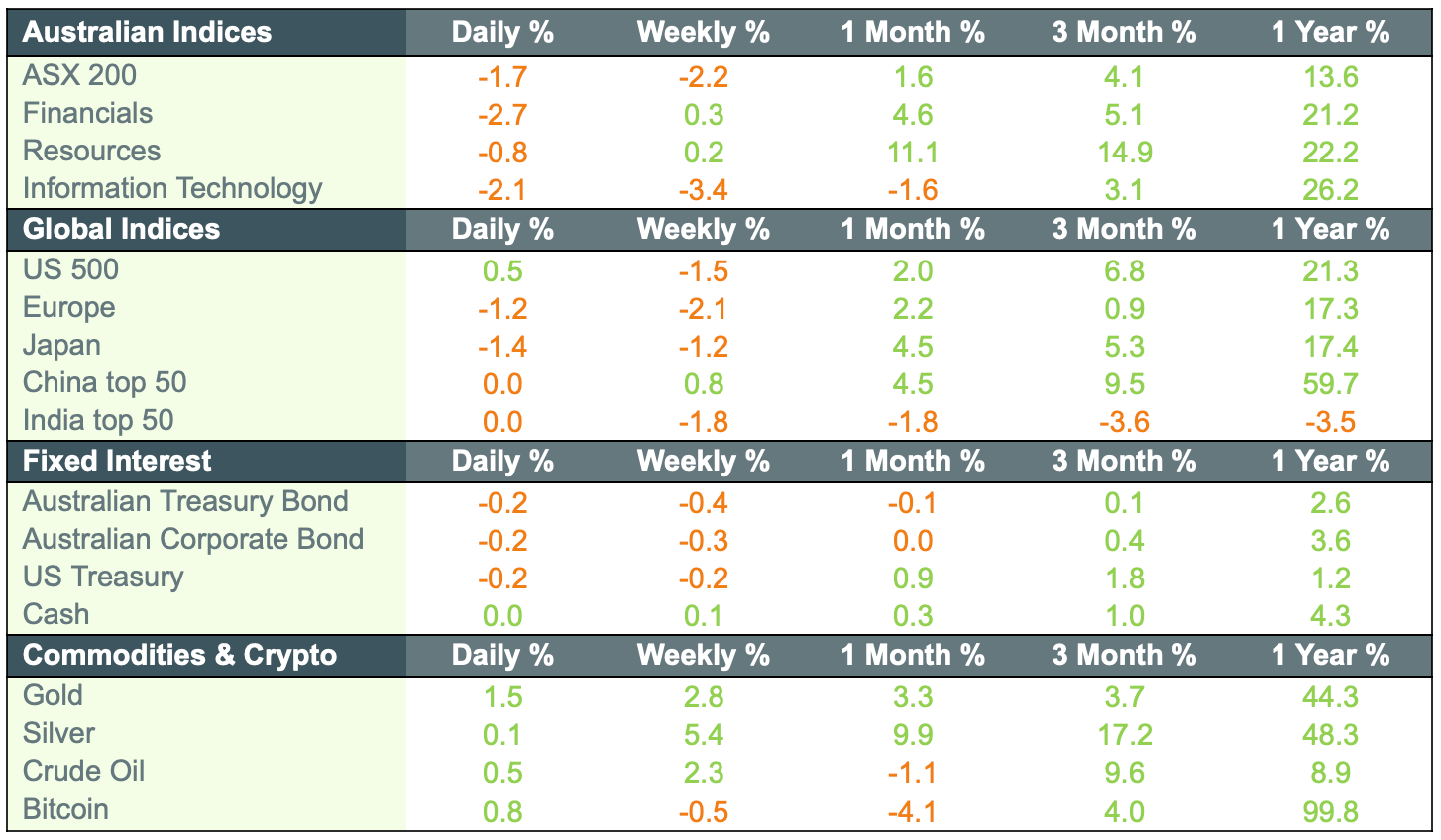

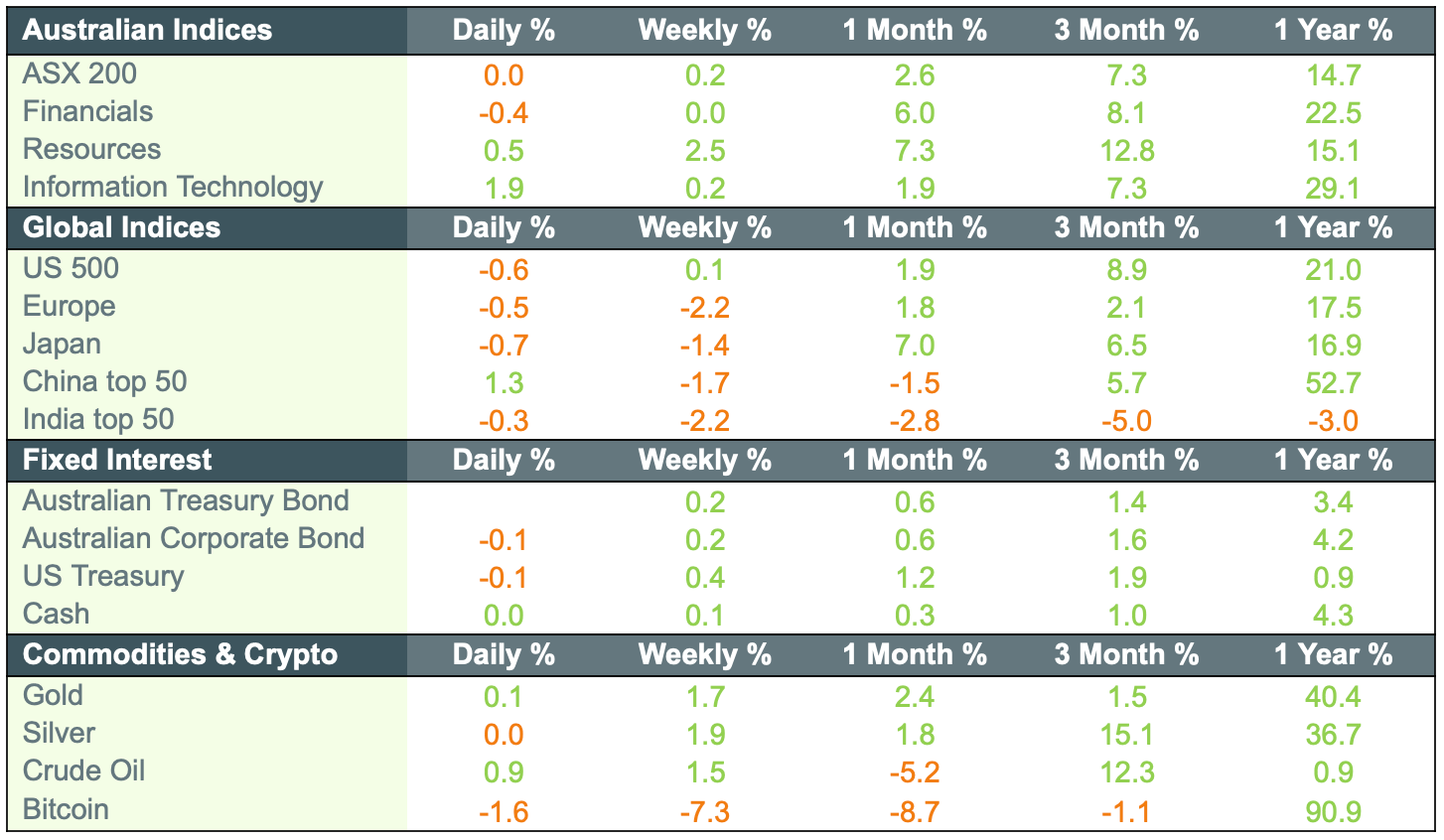

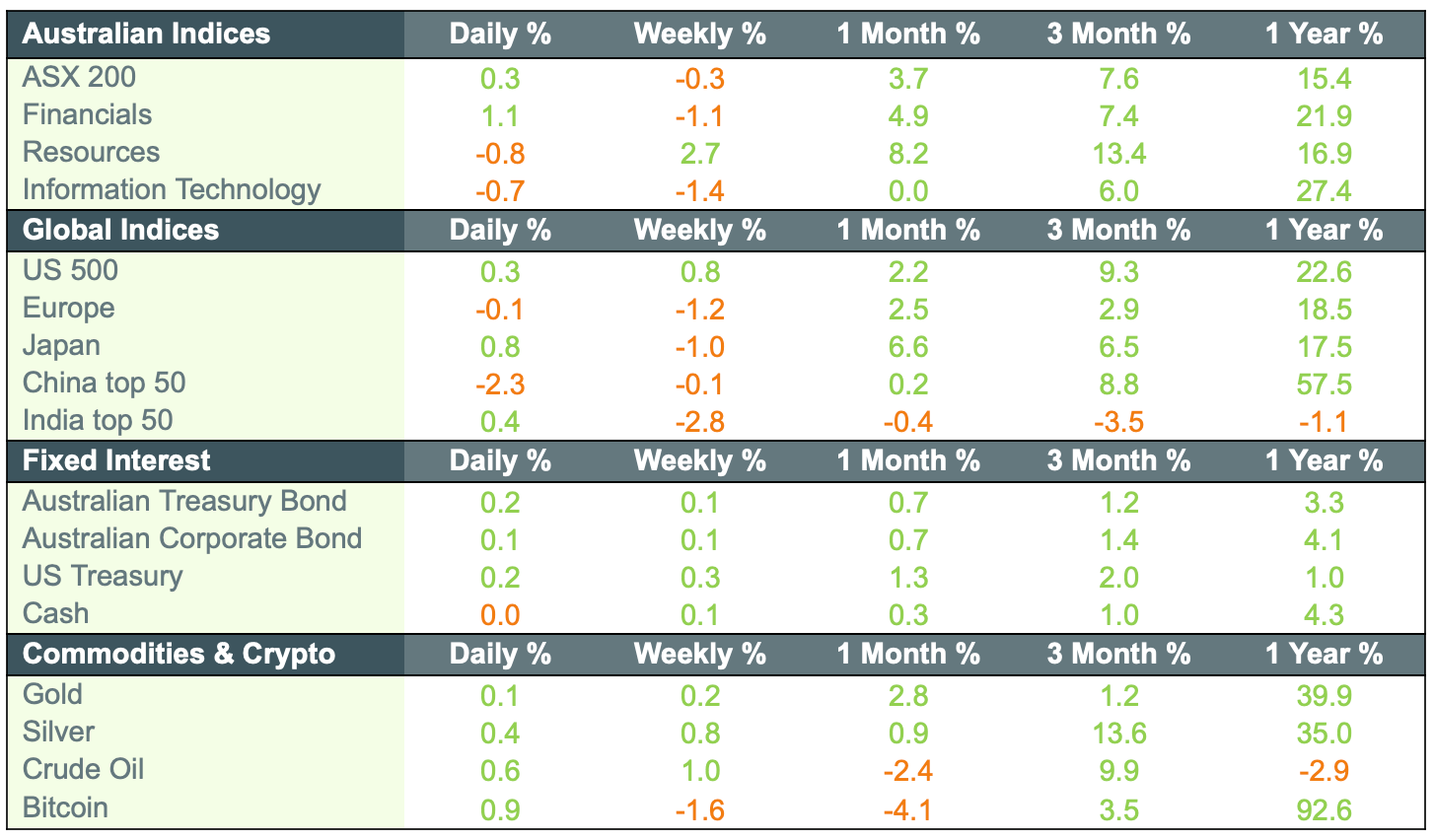

Market movements