Daily Market Update: 29 May, 2025

The key takeaways from the last 24 hours

Energy rise fails to carry index

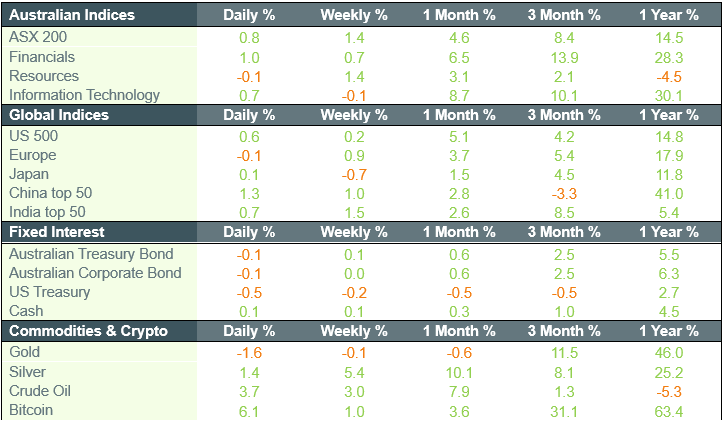

The benchmark Standard & Poor’s/ASX 200 Index (ASX: XJO) slid 10.7 points, or 0.1 per cent, to 8396.9, remaining within 2 per cent of its February high-water mark; while the All Ordinaries Index (ASX: XAO) walked back 6.6 points, to 8624.9. Six sectors rose, and five retreated. Energy was the standout, with the sector index rising 2.2 per cent, led by Woodside Energy Group Ltd (ASX: WDS), which advanced 69 cents, or 3.2 per cent, to $22.12 after its North-West Shelf project extension plan was approved by the federal government. Santos Limited (ASX: STO) firmed 12 cents, or 1.9 per cent, to $6.55; and Brazilian-based producer Karoon Energy Ltd (ASX: KAR) advanced 2.5 cents, or 1.5 per cent, to $1.66. Coal was also strong, with Whitehaven Coal Limited (ASX: WHC) gaining 15 cents, or 2.7 per cent, to $5.68; Yancoal Australia Ltd (ASX: YAL) appreciating 8 cents, or 1.5 per cent, to $5.32; Stanmore Resources Limited (ASX: SMR) gaining 4 cents, or 2.1 per cent, to $1.975; and New Hope Corporation Limited (ASX: NHC) adding 7 cents, or 1.9 per cent, to $3.84. Mineral Resources Limited (ASX: MIN), which mines iron ore and lithium, dropped $1.30, or 5.5 per cent, to $22.45 after another cut to its full-year guidance for iron ore production, this time by as much as 10 per cent. In gold, Westgold Resources Limited (ASX: WGX) lifted 8 cents, or 2.7 per cent, to $3.00; while Genesis Minerals Limited (ASX: GMD) advanced 6 cents, or 1.4 per cent, to $4.48; Ramelius Resources Limited (ASX: RMS) put on 3 cents, or 1.1 per cent, to $2.80; Perseus Mining Limited (ASX: PRU) was up 4 cents, also 1.1 per cent, to $3.80; and Newmont Corporation (NYSE: NEM) gained 66 cents, or 0.8 per cent, to $82.04. Copper miner Sandfire Resources Ltd (ASX: SFR) firmed 26 cents, or 2.3 per cent, to $11.62, while in uranium, Namibia-based producer Paladin Energy Ltd (ASX: PDN) gained 16 cents, or 2.5 per cent, to $6.46, while Canadian project developer NexGen Energy Ltd (TSX: NXE) added 5 cents, or 0.5 per cent, to $9.80.

Block boosts the tech sector, but banks slide

ASX technology shares were buoyant, led by Afterpay’s parent Block Inc. (NYSE: SQ), which surged $4.46, or 4.9 per cent, to $96.19; data centre operator NEXTDC Limited (ASX: NXT), which gained 31 cents, or 2.4 per cent, to $13.29; and enterprise software firm TechnologyOne Limited (ASX: TNE), which rose 94 cents, also 2.4 per cent, to $40.06. Banks turned downward after earlier gains. Index heavyweight Commonwealth Bank of Australia (ASX: CBA) lost $1.55, or 0.9 per cent, to $173.79. That trend extended to National Australia Bank Limited (ASX: NAB), which walked back 41 cents, or 1.1 per cent, to $37.34; Australia and New Zealand Banking Group Limited (ASX: ANZ), which dipped 18 cents, or 0.6 per cent, to $28.88; and Westpac Banking Corporation (ASX: WBC), which softened 31 cents, or 1 per cent, to $31.47. Macquarie Group Limited (ASX: MQG) eased 1 cent, to $209.99. Web Travel Limited (ASX: WEB) leapt 58 cents, or 12.4 per cent, to $5.26 after reporting a surge in bookings and total transaction value, saying it was back on track. Fisher & Paykel Healthcare Corporation Limited (ASX: FPH) fell $1.63, or 4.8 per cent, to $32.49 as investors shrugged off the company’s 43 per cent rise in full-year net profit. Testing, assaying and environmental monitoring company ALS Limited (ASX: ALQ) retreated $1.34, or 7.6 per cent, to $16.30 after it placed 21 million new shares with institutional investors, raising $350 million.

NVIDIA comes through with the goods, after hours

Stocks slipped on Wednesday as investors parsed earnings reports and Federal Reserve meeting minutes while awaiting NVIDIA Corporation’s (NASDAQ: NVDA) quarterly earnings. The benchmark Standard & Poor’s 500 Index (INDEXSP: .INX) slid 32.99 points, or 0.6 per cent, to 5888.55; the Dow Jones Industrial Average (INDEXDJX: .DJI) retreated 244.95 points, also 0.6 per cent, to 42,098.7; and the Nasdaq Composite Index (INDEXNASDAQ: .IXIC) walked back 98.23 points, or 0.5 per cent, to 19,100.94. HP Inc. (NYSE: HPQ) reported better-than-expected revenue but missed on earnings and issued disappointing guidance, sending its shares down 15 per cent. The Federal Reserve released the minutes from its May meeting, indicating continued caution and warning of potential “difficult trade-offs” if inflation rises. Bond markets responded, with the 30-year U.S. Treasury yield briefly hitting the 5 per cent level.

After the close, NVIDIA Corporation (NASDAQ: NVDA) reported earnings that beat expectations across revenue and profit lines, with 73 per cent year-on-year growth in its data centre business. The stock spiked more than 4 per cent in after-hours trading, immediately boosting index futures across the big three indices.

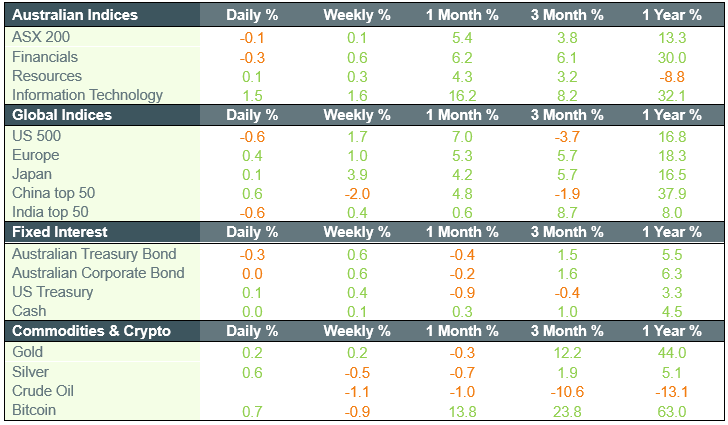

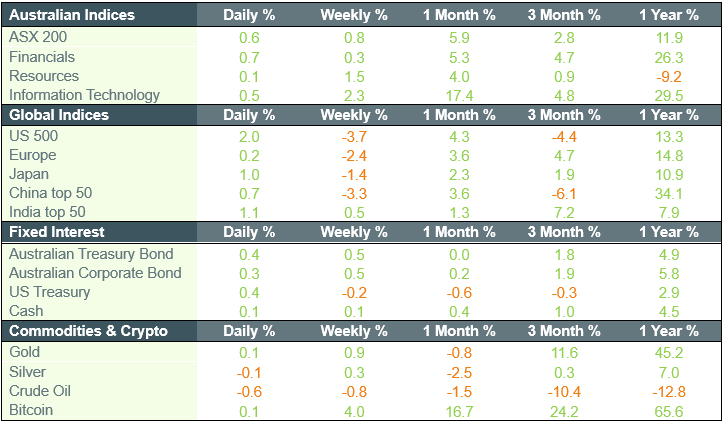

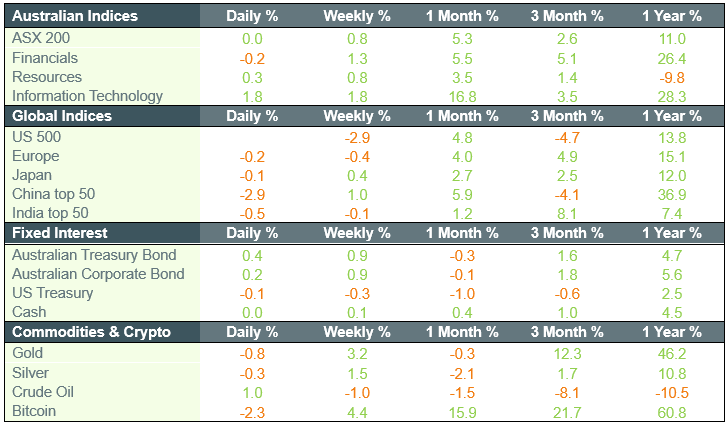

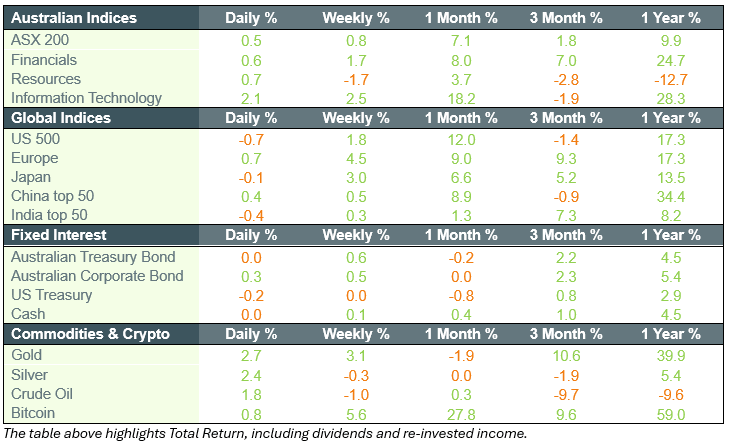

Market movements