The Australian share market ended Tuesday largely unchanged, with the S&P/ASX 200 Index dipping slightly by 1.2 points to 8541.1 as investors waited on developments in US trade negotiations. Financial markets remained cautious after US Treasury Secretary Scott Bessent warned tariffs could revert to earlier levels if deals aren’t made by the July 9 deadline. Canada’s suspension of its digital services tax and the European Union’s openness to a universal tariff highlight the rising urgency. The local technology sector took cues from the strong Nasdaq performance, with Xero Limited (ASX: XRO), Life360 Inc (ASX: 360), and Appen Limited (ASX: APX) all posting gains.

Real estate gains, HMC Capital slumps

Real estate stocks were lifted by rate-cut expectations ahead of the Reserve Bank of Australia’s upcoming meeting, with Scentre Group (ASX: SCG), GPT Group (ASX: GPT), and Stockland Corporation Limited (ASX: SGP) all climbing. Meanwhile, Commonwealth Bank of Australia (ASX: CBA) dragged the index lower with a 1.2 per cent drop, despite other banks such as Australia and New Zealand Banking Group Limited (ASX: ANZ) and National Australia Bank Limited (ASX: NAB) posting gains. In corporate news, HMC Capital Limited (ASX: HMC) plunged 17.3 per cent after scrapping its renewable energy strategy, while Insignia Financial Ltd (ASX: IFL) jumped 5.2 per cent following interest from private equity firm CC Capital. Biotech stocks were also active, with Tetratherix Limited (ASX: TTX) surging 12.3 per cent and Mesoblast Limited (ASX: MSB) gaining 11.2 per cent on positive FDA developments.

Global markets mixed as trade and budget dominate

US markets had a mixed session following the Senate’s approval of President Trump’s budget bill. The S&P 500 Index and the Nasdaq Composite Indexslipped 0.1 per cent and 0.8 per cent respectively, while the Dow Jones Industrial Average rose by 400 points, buoyed by strong gains in UnitedHealth Group Incorporated (NYSE: UNH) and Amgen Inc. (NASDAQ: AMGN). Tech stocks lagged, notably Tesla Inc. (NASDAQ: TSLA), which fell 5.3 per cent after President Trump escalated tensions with CEO Elon Musk. US Federal Reserve Chair Jerome Powell maintained a cautious stance on interest rates, citing tariff-related inflation concerns, while stronger-than-expected May job openings supported a patient monetary approach.

The Australian share market rose on Monday, with the S&P/ASX 200 Index (ASX: XJO) adding 28.1 points to close at 8542.3, marking a 0.3 per cent increase. Investor sentiment was buoyed by positive developments in US trade negotiations, which also fuelled a rally in Wall Street markets. Locally, seven of the 11 sectors gained, with health and technology stocks leading the advance. CSL Limited (ASX: CSL) climbed 2.2 per cent, Pro Medicus Limited (ASX: PME) gained 1.6 per cent, and Sigma Healthcare Limited (ASX: SIG) rose 1.4 per cent. The technology sector also saw strong performances, including a 2.2 per cent increase in NextDC Limited (ASX: NXT). Financials were mixed, with Macquarie Group Limited (ASX: MQG) up 3.9 per cent, while Commonwealth Bank of Australia (ASX: CBA) slipped 0.3 per cent.

Company updates and market movers

In corporate developments, James Hardie Industries plc (ASX: JHX) surged 7.1 per cent following the approval of a US$14 billion acquisition by Azek Company Inc (NYSE: AZEK), prompting a shift in its primary listing to New York. Star Entertainment Group Limited (ASX: SGR)dropped 6.9 per cent after its Hong Kong investors raised doubts over the Queen’s Wharf project in Brisbane. Meanwhile, DroneShield Limited (ASX: DRO) fell 4.2 per cent despite recent contract wins. NIB Holdings Limited (ASX: NHF) jumped 9.4 per cent after UBS Group AG (SWX: UBSG) upgraded its rating to “buy”. Newly listed biotech Tetratherix Limited (ASX: TTX) closed its debut session 4.9 per cent higher at $3.02. Superloop Limited (ASX: SLC) rose 1 per cent after lifting its full-year earnings forecast above previous guidance.

Global markets buoyed by tech rally and trade progress

Global markets extended gains as investors welcomed easing trade tensions and robust tech performance. The S&P 500 Index (NYSE: SPX)and Nasdaq 100 Index (NASDAQ: NDX) both advanced 0.5 per cent, supported by record highs in Microsoft Corporation (NASDAQ: MSFT)and Meta Platforms Inc (NASDAQ: META). Canada’s move to withdraw its digital services tax contributed to improved sentiment around ongoing US trade negotiations. The focus remains on the July 9 deadline tied to US tariff policies, with hopes for more deals to avoid renewed trade friction. Meanwhile, falling Treasury yields and rising expectations of interest rate cuts from the Federal Reserve created a favourable backdrop for equities, with the S&P 500 notching its strongest quarterly performance since late 2023.

The Australian sharemarket’s benchmark index, the S&P/ASX 200 Index (ASX: XJO), notched its sixth winning week out of the past seven on Friday, finishing the week up 0.1 per cent after a rally on Tuesday following the Iran-Israel ceasefire. With one more day of trading left in the 2025 financial year, the S&P/ASX 200 Index (ASX: XJO) is on track to deliver an annual return of 13.9 per cent, including dividends.

However, Friday was a down day, with the benchmark S&P/ASX 200 Index (ASX: XJO) finishing Friday down 36.6 points, or 0.4 per cent, at 8,514.2, while the broader All Ordinaries Index (ASX: XAO) dropped 30 points, or 0.3 per cent, to 8,743.7.

The market was led by the materials sector, which rose 2.3 per cent, as iron ore prices lifted to US$94.50 a tonne.

BHP Group Limited (ASX: BHP) gained $1.41, or 3.9 per cent, to $108.97; Rio Tinto Limited (ASX: RIO) accrued $4.78, or 4.6 per cent, to $108.97; and Fortescue Ltd (ASX: FMG) added 53 cents, or 3.6 per cent, to $15.46.

Big banks come off

Each of the big four banks finished lower, with Commonwealth Bank of Australia (ASX: CBA) sliding $5.35, or 2.8 per cent, to $185.36; Westpac Banking Corporation (ASX: WBC) giving up 67 cents, or 1.9 per cent, to $33.90; Australia and New Zealand Banking Group Limited (ASX: ANZ) losing 54 cents, or 1.8 per cent, to $29.20; and National Australia Bank Limited (ASX: NAB) easing 63 cents, or 1.6 per cent, to $39.26.

The big industrials news was plumbing supplies giant Reece Limited (ASX: REH) plunging $3.24, or 18.7 per cent, to $14.12, giving up two-and-a-half years of gains. The company said that it expected to earn between $548 million and $558 million this financial year, down from $681 million it made in the 2024 financial year, and well below the $580 million the market was expecting.

US indices on track for strong June

On Wall Street on Friday, the broad S&P 500 Index (NYSE: SPX) touched its first new high since February, marking a 23 per cent rally from the depths of April’s tariff-induced sell-off. At its low in April, the S&P 500 was down nearly 18 per cent for 2025, but the index has taken just 89 trading days to to regain the lost ground. That makes it the US benchmark’s quickest recovery back to a record close, after a decline of at least 15 per cent, in its history, according to Dow Jones Market Data.

The S&P 500 Index (NYSE: SPX) gained 32.05 points, or 0.5 per cent, at 6,173.07, surpassing its previous record of 6,147.43. At its low in April, the S&P 500 Index (NYSE: SPX) was down nearly 18 per cent for the year when global trade and tariff tensions spooked the market.

The technology-focused Nasdaq Composite Index (NASDAQ: IXIC) also hit an all-time high, adding 105.54 points, or 0.5 per cent, to 20,273.46, while the blue-chip Dow Jones Industrial Average (NYSE: DJI) added 432.43 points, or 1 per cent, to 43,819.27.

For June, the S&P 500 Index (NYSE: SPX) is up 4.4 per cent, while the Nasdaq Composite Index (NASDAQ: IXIC) has surged nearly 6.1 per cent, and the Dow Jones Industrial Average (NYSE: DJI) has put on about 3.7 per cent.

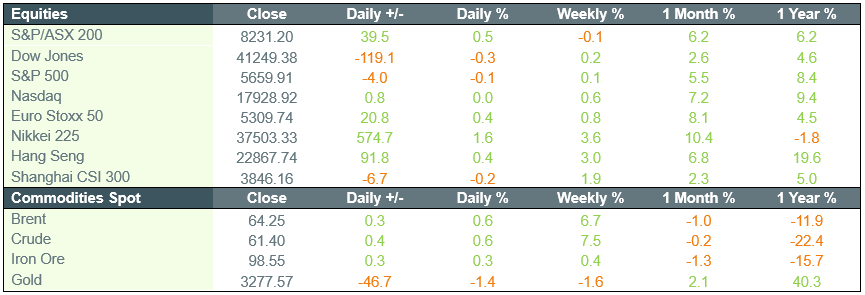

The Australian share market closed higher on Friday but logged its first weekly decline since early April, as a late rebound in financial stocks failed to offset the broader sell-off earlier in the week. The S&P/ASX 200 Index gained 0.5 per cent, or 39.5 points, to finish at 8231.2. However, it slipped 0.1 per cent over the five-day period, weighed down by lacklustre earnings reports from Westpac Banking Corporation (ASX: WBC) and Australia and New Zealand Banking Group Limited (ASX: ANZ). On Friday, nine of the 11 sectors closed in positive territory, with banks and technology stocks leading the gains.

Global sentiment was lifted by a new US-UK trade framework aimed at reducing or eliminating tariffs on exports such as steel, aluminium, and automobiles. Optimism around potential progress in US-China trade relations, ahead of planned talks in Switzerland between United States Treasury Secretary Scott Bessent and Chinese officials, also supported commodity markets. Iron ore and oil prices advanced, and Bitcoin hovered above $US103,000—a three-month high. In Australia, Macquarie Group Limited (ASX: MQG) surged 3.8 per cent to $203.31 after reporting a near 6 per cent lift in full-year profit. Commonwealth Bank of Australia (ASX: CBA) rose 0.9 per cent to $167.04, while Australia and New Zealand Banking Group Limited (ASX: ANZ) declined.

Stocks in focus

Several individual stocks made notable moves in Friday’s session. In corporate news, CoStar Group Inc. (NASDAQ: CSGP) finalised a $3 billion acquisition of Domain Holdings Australia Limited (ASX: DHG), boosting Domain’s share price 3.1 per cent to $4.38. Its majority owner, Nine Entertainment Co. Holdings Limited (ASX: NEC), jumped 6 per cent to $1.58.

Healthcare firm Healius Limited (ASX: HLS) posted the day’s largest loss, falling 25 per cent to $1.16 after trading ex-dividend. REA Group Limited (ASX: REA) dipped 2 per cent to $244.97 despite an 18 per cent increase in commercial revenue over the nine months to March. Meanwhile, Chrysos Corporation Limited (ASX: C79) soared 17.9 per cent to $4.87 after signing a deal with Newmont Corporation (NYSE: NEM) to roll out its minerals analysis technology across Newmont’s global operations.

Us stocks end mixed as trade talks loom

U.S. equity markets closed with mixed results on Friday, as investors remained cautious ahead of high-level trade negotiations between the United States and China. The S&P 500 Index dipped 0.1 per cent to 5,659.91, while the Dow Jones Industrial Average fell 0.3 per cent to 41,249.38. The Nasdaq Composite Index was nearly unchanged, edging up 0.78 points to 17,928.92. For the week, all three major indices posted modest gains, with the S&P 500 up 0.1 per cent, the Dow Jones down 0.2 per cent, and the Nasdaq Composite up 0.6 per cent.

Among key movers, Tesla Inc. (NASDAQ: TSLA) surged 4.3 per cent to $297.19 after climbing above its 200-day moving average, marking a potential buying opportunity for aggressive investors. Apple Inc. (NASDAQ: AAPL) rose 0.53 per cent to $198.53, with analysts maintaining a positive outlook on its AI initiatives. Amazon.com Inc. (NASDAQ: AMZN) gained 0.51 per cent to $192.50, supported by growth in its advertising business. In semiconductors, Texas Instruments Inc. (NASDAQ: TXN) climbed 4.0 per cent to $172.27, outperforming peers.

With investors on the sidelines, waiting to see whether the fragile cease-fire between Israel and Iran will hold, there was not much in the way of index movement in the Wednesday session on the Australian Securities Exchange (ASX), with the benchmark S&P/ASX 200 Index (ASX: XJO) closing up 3.7 points at 8,559.20, and the broader All Ordinaries Index (ASX: XAO) accruing 5.1 points to 8,779. The ‘story’ for the day was Commonwealth Bank of Australia (ASX: CBA) hitting yet another record high, gaining $3.27, or 1.7 per cent, to $191.40. The stock is now up almost 25 per cent in 2025 so far, and trades at more than 30 times expected FY26 earnings, making it arguably the most expensively rated bank in the world. The big four Australian banks normally trade on about 12–13 times earnings. Of its peers, Australia and New Zealand Banking Group Limited (ASX: ANZ) lifted 50 cents, or 1.8 per cent, to $29.10; National Australia Bank Limited (ASX: NAB) picked up 30 cents, or 0.8 per cent, to $40.05; and Westpac Banking Corporation (ASX: WBC) added 25 cents, or 0.7 per cent, to $34.54.

Newly refloated airline Virgin Australia Holdings Limited (ASX: VGN) followed its strong debut yesterday—when it rose 11.4 per cent above the $2.90 issue price—with a gain of 11 cents, or 3.4 per cent, to $3.34. Equipment-financier and consumer buy-now-pay-later company Humm Group Limited (ASX: HUM) spiked 5.5 cents, or 11.5 per cent, higher to 54 cents after the company confirmed a takeover offer from the family office of its chairman, Andrew Abercrombie. Counter-drone-technology company DroneShield Limited (ASX: DRO) surged 35.5 cents, or 19.9 per cent, to $2.15 after being awarded its biggest-ever defence order — a package of three contracts worth $61.6 million, with the end-buyer being a European military customer. The contracts are for handheld detection and counter-drone systems and associated accessories. The order’s value is larger than the entire $57.5 million revenue DroneShield Limited (ASX: DRO) generated in 2024.

In economic news, the Australian Bureau of Statistics (ABS) reported a fall in annual trimmed-mean inflation in May to 2.4 per cent—its lowest level since November 2021—which led some bank economists to forecast a rate cut next month.

Resources screens mostly red

Among the big miners, BHP Group Limited (ASX: BHP) eased 37 cents, or 1 per cent, to $36.11; Rio Tinto Limited (ASX: RIO) slipped 64 cents, or 0.6 per cent, to $104.30; and Fortescue Metals Group Limited (ASX: FMG) gave up 35 cents, or 2.3 per cent, to $14.88. In energy, Woodside Energy Group Limited (ASX: WDS) surrendered 16 cents, or 0.7 per cent, to $24.00 despite sealing a US$5.7 billion deal over its Louisiana LNG project, while Santos Limited (ASX: STO) lost 9 cents, or 1.2 per cent, to $7.57.

In coal, Whitehaven Coal Limited (ASX: WHC) walked back 12 cents, or 2.2 per cent, to $5.45; New Hope Corporation Limited (ASX: NHC) shed 10 cents, or 2.6 per cent, to $3.75; and Stanmore Resources Limited (ASX: SMR) fell 9 cents, or 4.7 per cent, to $1.83. Mineral Resources Limited (ASX: MIN), which mines lithium and iron ore, slipped $1.28, or 6 per cent, to $20.18; lithium producer Pilbara Minerals Limited (ASX: PLS) lost 4 cents, or 3.1 per cent, to $1.25; and diversified miner South32 Limited (ASX: S32) eased 8 cents, or 2.7 per cent, to $2.84.

In gold, Capricorn Metals Limited (ASX: CMM) fell 49 cents, or 4.7 per cent, to $9.90; Genesis Minerals Limited (ASX: GMD) softened 18 cents, or 4 per cent, to $4.34; Perseus Mining Limited (ASX: PRU) slid 12 cents, or 3.4 per cent, to $3.37; and Northern Star Resources Limited (ASX: NST) gave up 52 cents, or 2.6 per cent, to $19.28. Green arrows were rare on the resources screens, but Namibia-based uranium producer Paladin Energy Limited (ASX: PDN) firmed 26 cents, or 3.5 per cent, to $7.75; Capstone Copper Corp. (TSX: CS) gained 9 cents, or 1 per cent, to $8.95; Canadian-based uranium project developer NexGen Energy Ltd. (ASX: NXG) advanced 8 cents, or 0.8 per cent, to $10.42; and gold miner Gold Road Resources Limited (ASX: GOR) lifted 2 cents, or 0.6 per cent, to $3.33.

White House, Fed differ on rate cuts

In the US, tensions in the Middle East appeared to be calming, and investors are preparing for May’s personal-consumption-expenditures price-index reading, which will be released on Friday. The broad S&P 500 Index (INDEXSP: SPX) finished Wednesday’s session flat, minutely lower at 6,092.16, while the 30-stock Dow Jones Industrial Average (INDEXDJX: DJI) slid 106.59 points, or 0.3 per cent, to 42,982.43; but the Nasdaq Composite Index (NASDAQ: IXIC) appreciated 61.02 points, or 0.3 per cent, to 19,973.55, edging closer to a new record. The Nasdaq was powered by chipmaker NVIDIA (NASDAQ: NVDA), which jumped 4.3 per cent, touching a record high and lifting its market capitalisation to US$3.75 trillion, making it the world’s most valuable company.

Federal Reserve Chair Jerome Powell said this week that the central bank’s preferred inflation measure is likely to rise to 2.3 per cent, while the ‘core’ figure, which excludes food and energy, is expected to tick up to 2.6 per cent from 2.5 per cent in April. However, Powell stressed that the central bank is committed to keeping inflation under control in the face of “uncertain” effects of Trump’s tariffs on the economy: while the White House is demanding rate cuts, the Federal Reserve chair is determined to wait to see the impact on inflation—rate-cut decisions will be based on that.

What turmoil, says Commonwealth Bank of Australia?

The local market headed lower as investors weighed concerns about the escalating conflict in the Middle East, but the negative sentiment was not able to put a dent in the rise of Commonwealth Bank of Australia (ASX: CBA). The benchmark S&P/ASX 200 Index (ASX: XJO) gave up 30.6 points, or 0.4 per cent, to 8,474.90 points on Monday; and the broader All Ordinaries Index (ASX: XAO) lost 35.5 points, also 0.4 per cent, to 8,688; but Commonwealth Bank of Australia (ASX: CBA) gained another $1.82, or 1 per cent, to $184.35 – after setting a new intra-day record at $184.41. Offshore investors can’t seem to get enough of the nation’s biggest bank. Not all of the other big banks rode on Commonwealth Bank of Australia (ASX: CBA)’s coat-tails: Westpac Banking Corporation (ASX: WBC) put on 21 cents, or 0.6 per cent, to $33.42; but Australia and New Zealand Banking Group Limited (ASX: ANZ) eased 18 cents, or 0.6 per cent, to $28.21; and National Australia Bank Limited (ASX: NAB) softened 3 cents, to $38.88. Elsewhere in the industrial world, Qantas Airways Limited (ASX: QAN) slipped 19 cents, or 1.9 per cent, and global logistics giant Brambles Limited (ASX: BXB) gave up $1.23, or 5 per cent, to $23.33. Adairs Limited (ASX: ADH) sank 53 cents, or 20.5 per cent, to $2.05 after warning that full-year earnings would come in below last year’s. It said that while stronger promotional activity had boosted sales, it would dent margins. The news spooked investors in rival retailer Temple & Webster Group Limited (ASX: TPW), which shed 48 cents, or 2.3 per cent, to $20.87; JB Hi-Fi Limited (ASX: JBH)fell 30 cents, or 0.3 per cent, to $108.40; but furniture heavyweight Nick Scali Limited (ASX: NCK) advanced 19 cents, or 1 per cent, to $18.33.

Resources mostly lower

In the energy sector, Santos (ASX: STO) added one per cent, while Woodside (ASX: WDS) was flat as Brent crude rose $US2 over the Australian session to over $US78 a barrel, near its highest level since late January. In big mining, BHP Group Limited (ASX: BHP) retreated 57 cents, or 1.6 per cent, to $35.64; Rio Tinto Limited (ASX: RIO) slipped 34 cents, or 0.3 per cent, to $101.83; and Fortescue Ltd (ASX: FMG) walked back 15 cents, or 1 per cent, to $14.54. Elsewhere in resources, gold miner West African Resources Limited (ASX: WAF) gained 4 cents, or 1.8 per cent, to $2.21; fellow gold producer Newmont Corporation (NYSE: NEM) lifted $1.07, or 1.2 per cent, to $90.37; North American-based Capstone Copper Corp. (TSE: CS) gained 12 cents, or 1.4 per cent, to $8.57; and Namibia-based uranium producer Paladin Energy Limited (ASX: PDN) advanced 6 cents, or 0.8 per cent, to $7.42. But at the other end of the spectrum, gold miner Genesis Minerals Limited (ASX: GMD) dropped 18 cents, or 3.9 per cent, to $4.43; coal producer Whitehaven Coal Limited (ASX: WHC) lost 20 cents, or 3.5 per cent, to $5.57; gold miner Northern Star Resources Limited (ASX: NST) fell 64 cents, or 3.1 per cent, to $19.88; fellow goldie Capricorn Metals Ltd (ASX: CMM) shed 32 cents, or 3 per cent, to $10.20; Ramelius Resources Limited (ASX: RMS), also a gold miner, leaked 8 cents, or 3 per cent, to $2.58; Canadian-based Champion Iron Limited (ASX: CIA) slid 12 cents, or 3 per cent, to $3.95; and Indonesia-based nickel producer Nickel Industries Limited (ASX: NIC) lost 2 cents, or 2.8 per cent, to 70 cents.

US markets rally, but big news comes after close

Overnight, US markets rallied as Iran did not close the Strait of Hormuz, a crucial oil shipping route; also, prospects of the United States Federal Reserve cutting interest rates as early as July contributed to the upbeat mood. The market also shrugged off Iranian missile attacks on US bases in Qatar and Iraq, which did not cause any reported casualties, mainly because Iran gave the US advance notice of the missile strikes. Despite the attack, the US markets moved higher, with the broad S&P 500 Index (NYSEARCA: SPY) gaining 57.33 points, or 1 per cent, to 6,025.17; the blue-chip Dow Jones Industrial Average (INDEXDJX: DJI) adding 374.96 points, or 0.9 per cent, to 42,581.78; and the tech-heavy Nasdaq Composite Index (NASDAQ: IXIC) rising 183.57 points, also up 0.9 per cent, to 19,630.98. Bonds also rallied, with the US 10-year treasury trading 4 basis points lower at 4.34 per cent and at the short end, the two-year yielding 3.85 per cent, down 6 basis points. The major impact of Middle East events was felt in the oil price, which fell 7 per cent after Iran’s subdued response, and restraint on the Strait of Hormuz. After trading closed, US President Donald Trump announced an imminent ceasefire between Israel and Iran sent stock futures climbing, with Dow Jones Industrial Average (INDEXDJX: DJI) and S&P 500 Index (NYSEARCA: SPY) futures up about 0.4 per cent, and Nasdaq Composite Index (NASDAQ: IXIC) futures up about 0.6 per cent.

Australian market edges lower amid banking sector drag

The Australian share market declined for a fourth consecutive session, with the S&P/ASX 200 Index (ASX: XJO) falling 18.2 points, or 0.2 per cent, to close at 8505.5 — its lowest level since early June. The retreat came as investors adopted a cautious stance amid escalating geopolitical concerns, particularly regarding potential US involvement in the conflict between Israel and Iran. Six of the 11 market sectors closed in negative territory, leading to a modest weekly drop of 0.5 per cent for the benchmark index. The financial sector weighed heavily, with Commonwealth Bank of Australia (ASX: CBA), National Australia Bank Limited (ASX: NAB), Westpac Banking Corporation (ASX: WBC), and Australia and New Zealand Banking Group Limited (ASX: ANZ) all recording losses.

Healthcare gains and mining divergence

In contrast, defensive sectors saw renewed investor interest. Healthcare stocks performed strongly, with Pro Medicus Limited (ASX: PME), ResMed Inc. (ASX: RMD), and Cochlear Limited (ASX: COH) all posting gains, the latter climbing 2.5 per cent to $295.64. The mining sector delivered mixed results following a Citi downgrade of lithium price forecasts. Liontown Resources Limited (ASX: LTR) rebounded slightly despite initial losses, while Pilbara Minerals Limited (ASX: PLS) and Mineral Resources Limited (ASX: MIN) fell sharply. In corporate developments, Betr rose 5.3 per cent after submitting an all-share bid to acquire PointsBet Holdings Limited (ASX: PBH), while Bowen Coking Coal Limited (ASX: BCB) plunged 48.6 per cent after warning of potential mine suspensions due to market conditions and state royalties.

US markets decline amid war fears

On the global front, the US500 Index (CBOE: SPX), the primary benchmark for US equities, fell to 5948 points on June 22, marking a 0.32 per cent decline from the previous session. The downturn was driven by rising geopolitical instability following reports that the United States carried out airstrikes on Iranian nuclear facilities, stoking investor concerns over a broader regional conflict. Despite the short-term dip, the index has climbed 2.21 per cent over the past month.

The Australian sharemarket ended marginally lower on Wednesday, with the S&P/ASX 200 Index (ASX: XJO) down 0.1 per cent to close at 8531.2. The modest dip came despite eight of the eleven industry sectors posting gains, as a sharp retreat in the materials sector weighed heavily on the broader market. The key driver of this decline was renewed pressure on iron ore prices, which slipped below $US93 a tonne in Singapore.

Iron ore slump hits major miners

Iron ore-exposed stocks bore the brunt of the market’s retreat, with BHP Group Limited (ASX: BHP) falling 1.2 per cent to $36.86, Fortescue Metals Group Limited (ASX: FMG) sliding 4 per cent to $15.03, and Mineral Resources Limited (ASX: MIN) tumbling 4.6 per cent to $22.59. Citi downgraded its 12-month forecast for iron ore prices to $US90 per tonne, adding further pressure. Gold miners also declined despite global tensions, with Northern Star Resources Limited (ASX: NST) dropping 2 per cent to $20.58 and Evolution Mining Limited (ASX: EVN)falling 3.6 per cent to $8.15. In contrast, uranium stocks rallied, with Boss Energy Limited (ASX: BOE) gaining 4.3 per cent after strong production results, and Deep Yellow Limited (ASX: DYL) advancing 3.9 per cent on speculation of higher uranium prices.

Global jitters amid Fed hold and Middle East unrest

On Wall Street, markets were mixed following the US Federal Reserve’s decision to leave interest rates unchanged. The S&P 500 Index (NYSE: SPX) dipped slightly, the Dow Jones Industrial Average (NYSE: DJI) fell 44 points, while the Nasdaq Composite Index (NASDAQ: IXIC) inched up 0.1 per cent. Fed Chair Jerome Powell maintained a cautious tone, highlighting uncertainty around inflation and growth, while signaling two potential rate cuts in 2025. Rising geopolitical risks, particularly from escalating tensions between Israel and Iran, added to investor unease and pushed oil prices higher. Meanwhile, payment stocks Visa Inc (NYSE: V), Mastercard Inc (NYSE: MA), and PayPal Holdings Inc (NASDAQ: PYPL) each dropped over 4 per cent following the passage of the US Congress’s stablecoins act.

ASX retreats as geopolitical tensions stir investor caution

The Australian share market closed marginally lower on Tuesday as geopolitical risks overshadowed an initial positive start. The S&P/ASX 200 Index (ASX: XJO) dipped by 7.1 points to finish at 8541.3, despite tracking earlier gains from Wall Street. The volatility was sparked by former US President Donald Trump’s unexpected social media call for the evacuation of Tehran, raising market jitters across Asia. Investor sentiment remained cautious as seven of the 11 sectors on the ASX ended in the red, with Commonwealth Bank of Australia (ASX: CBA) and BHP Group Limited (ASX: BHP) both edging lower by 0.2 per cent and 0.4 per cent, respectively.

Gold, uranium stocks lift as safe haven demand rises

Gold-related equities saw strong performances amid growing market uncertainty. Newmont Corporation (ASX: NEM) gained 2.5 per cent and Northern Star Resources Limited (ASX: NST) climbed 1.5 per cent, mirroring a spike in global gold prices to $US3394.68 per ounce. Uranium stocks also surged as hedge funds scrambled to cover short positions, following news of a $US100 million capital raise by the Sprott Physical Uranium Trust. Gains included Deep Yellow Limited (ASX: DYL) up 5.7 per cent, Boss Energy Limited (ASX: BOE) up 3.2 per cent, Silex Systems Limited (ASX: SLX) up 3 per cent, and Paladin Energy Limited (ASX: PDN) up 4.4 per cent. Santos Limited (ASX: STO) added 0.5 per cent following ongoing speculation over a potential $30 billion takeover bid.

Wall Street slips amid Middle East tensions and weak data

Global markets were pressured by rising Middle East tensions and disappointing economic indicators. The S&P 500 Index (NYSE: SPX) dropped 0.8 per cent, the Dow Jones Industrial Average (NYSE: DJI) fell 299 points, and the Nasdaq Composite Index (NASDAQ: IXIC)declined 0.9 per cent. Investor anxiety grew following Trump’s threats of potential strikes on Iran and calls for its “unconditional surrender”. Adding to the negative sentiment, US retail sales fell 0.9 per cent in May, suggesting weakening consumer demand. Among stocks, JetBlue Airways Corporation (NASDAQ: JBLU) plummeted 7.9 per cent on weak travel demand outlook, while ExxonMobil Corporation (NYSE: XOM) and Chevron Corporation (NYSE: CVX) rose 1.3 per cent and 3.2 per cent respectively, driven by a surge in oil prices.

The Australian share market remained resilient on Monday, navigating geopolitical uncertainty and a sell-off in the United States by edging slightly higher. The benchmark S&P/ASX 200 Index (ASX: XJO) ended the day up just 1 point at 8548.4 points, supported by a strong rally in energy shares following a sharp spike in oil prices and confirmation of a $30 billion takeover of Santos Limited (ASX: STO). Other oil stocks rose in tandem, with Woodside Energy Group Limited (ASX: WDS) up 3 per cent to $26, Beach Energy Limited (ASX: BPT) gaining 1.9 per cent to $1.33, and Karoon Energy Limited (ASX: KAR) climbing 2.3 per cent to $2.03. Meanwhile, uranium shares also spiked after news that the Sprott Physical Uranium Trust (TSX: U.UN) would raise $US100 million to purchase uranium. Shares in Deep Yellow Limited (ASX: DYL) surged 21.2 per cent to $1.60, Paladin Energy Limited (ASX: PDN) rose 15.6 per cent to $7.30, Boss Energy Limited (ASX: BOE) gained 17.7 per cent to $4.30, and Silex Systems Limited (ASX: SLX) soared 23.9 per cent to $4.

Financials and gold weigh on broader market

Despite energy’s strong performance, broader gains were capped by weakness in financials and gold stocks. Commonwealth Bank of Australia (ASX: CBA) slipped 0.03 per cent to $179.40, while National Australia Bank Limited (ASX: NAB), Westpac Banking Corporation (ASX: WBC) and Australia and New Zealand Banking Group Limited (ASX: ANZ) also declined. Among gold miners, Evolution Mining Limited (ASX: EVN) dropped 8 per cent to $8.45 after UBS Group AG (SWX: UBSG) downgraded it to a “sell”, and Northern Star Resources Limited (ASX: NST) fell 8.2 per cent to $20.68 following a downgrade to “neutral”. ASX Limited (ASX: ASX) declined 6.7 per cent to $67.90 after Australian Securities and Investments Commission (ASIC) launched an inquiry into its governance practices. In contrast, Bubs Australia Limited (ASX: BUB) rose 6.3 per cent to 17 cents on US regulatory progress, while Tourism Holdings Limited (ASX: THL) soared 56 per cent to $2.10 after receiving a $471 million buyout offer from BGH Capital and the Trouchet brothers.

Wall Street rises despite Middle East tensions

United States markets rebounded on Monday ahead of the United States Federal Reserve’s policy decision. The S&P 500 Index (NYSE: SPX) rose 0.9 per cent, the Dow Jones Industrial Average (NYSE: DJI) gained 0.7 per cent, and the Nasdaq Composite Index (NASDAQ: IXIC) jumped 1.4 per cent. Hopes of de-escalation between Iran and Israel supported gains, particularly in tech and consumer stocks, with Meta Platforms Inc. (NASDAQ: META), Palantir Technologies Inc. (NYSE: PLTR), and Tesla Inc. (NASDAQ: TSLA) all advancing. Energy shares lagged as oil prices fell. Meanwhile, United States Steel Corporation (NYSE: X)climbed 5.1 per cent after approval of its sale to Nippon Steel Corporation (TYO: 5401), and Roku Inc. (NASDAQ: ROKU) soared 10.4 per cent on a new advertising deal with Amazon Ads, part of Amazon.com Inc. (NASDAQ: AMZN).