Daily Market Update: 14 August, 2025

The key takeaways from the last 24 hours

CBA sell-off weighs on local market

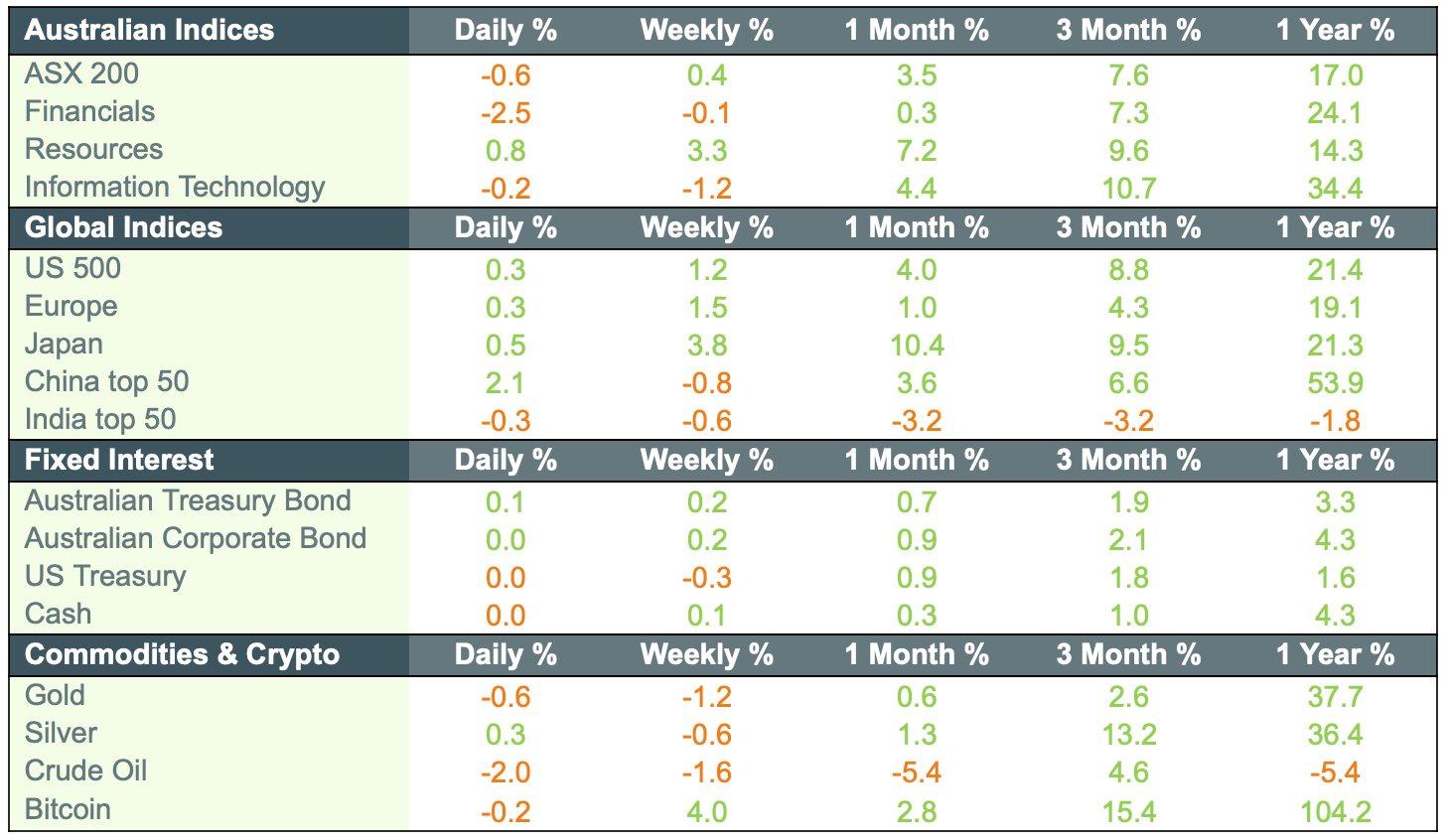

The Australian sharemarket posted its sharpest one-day decline in two weeks, dragged lower primarily by a sell-off in Commonwealth Bank of Australia (ASX: CBA). The S&P/ASX 200 Index (ASX: XJO) fell 53.70 points to close at 8827.10, a drop of 0.6 per cent after touching a record high at the open. The decline followed a rate cut by the Reserve Bank of Australia and softer US inflation data, which bolstered global rate cut expectations. CBA shares dropped 5.4 per cent to $169.12 despite reporting a $10.25 billion cash profit, as investors balked at its valuation near 30 times forward earnings. The weakness spread across the banking sector, with National Australia Bank Limited (ASX: NAB) down 2.6 per cent, Westpac Banking Corporation (ASX: WBC) off 2.1 per cent, and Australia and New Zealand Banking Group Limited (ASX: ANZ) finishing 0.2 per cent lower.

Rotation to healthcare and miners cushions broader losses

Investors shifted into defensives, with healthcare and mining sectors providing some support to the broader index. CSL Limited (ASX: CSL) climbed 2 per cent and Clarity Pharmaceuticals Limited (ASX: CU6) rose 5.3 per cent. Miners gained on the back of strong iron ore prices, with Fortescue Metals Group Limited (ASX: FMG) up 1.4 per cent, BHP Group Limited (ASX: BHP) rising 1.1 per cent, and Rio Tinto Limited (ASX: RIO) gaining 1 per cent. Meanwhile, AGL Energy Limited (ASX: AGL) slumped 13.1 per cent following a 21.2 per cent drop in core profit. Treasury Wine Estates Limited (ASX: TWE) added 1.2 per cent after lifting its dividend and announcing a share buyback. Insurance Australia Group Limited (ASX: IAG)slipped 0.1 per cent despite strong profit growth, while Tyro Payments Limited (ASX: TYR) surged 11.5 per cent on takeover interest.

Global rally sustained by rate cut hopes and Chinese momentum

Globally, equity markets extended gains as expectations grew for a September rate cut by the Federal Reserve, following soft US inflation data. The S&P 500 Index (NYSE: SPX) rose 0.3 per cent, the Nasdaq Composite Index (NASDAQ: IXIC) added 0.1 per cent, and the Dow Jones Industrial Average (NYSE: DJI) climbed 463 points. Gains were led by materials, healthcare, and consumer cyclicals, with Advanced Micro Devices Inc. (NASDAQ: AMD) jumping 5.4 per cent and Paramount Skydance surging 36.7 per cent. Meanwhile, China’s stock market continued its steady rebound, with the CSI 300 Index (SHA: 000300) up 16 per cent from April lows amid high liquidity and retail investor optimism, despite no major economic stimulus announcements from Beijing.

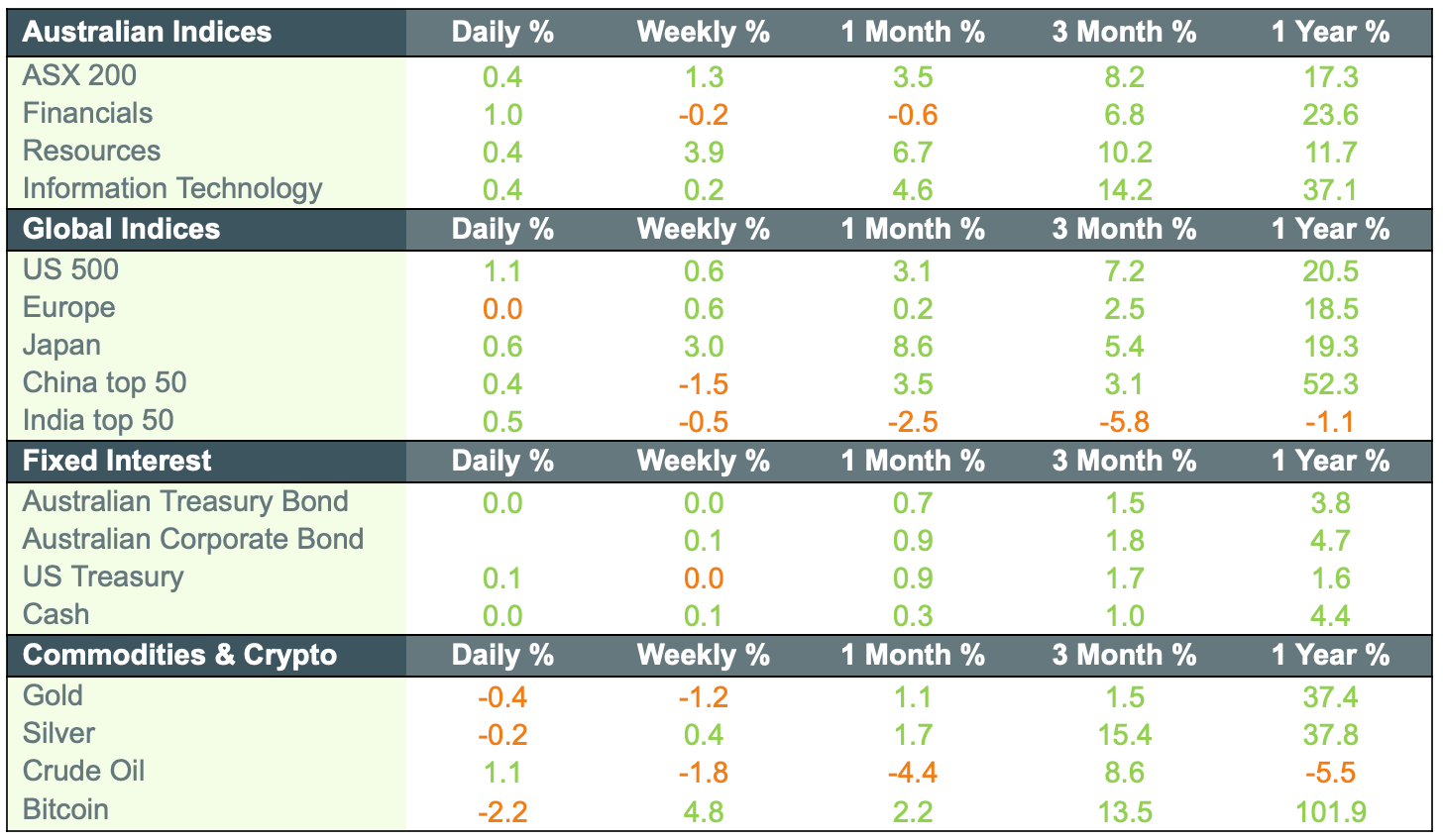

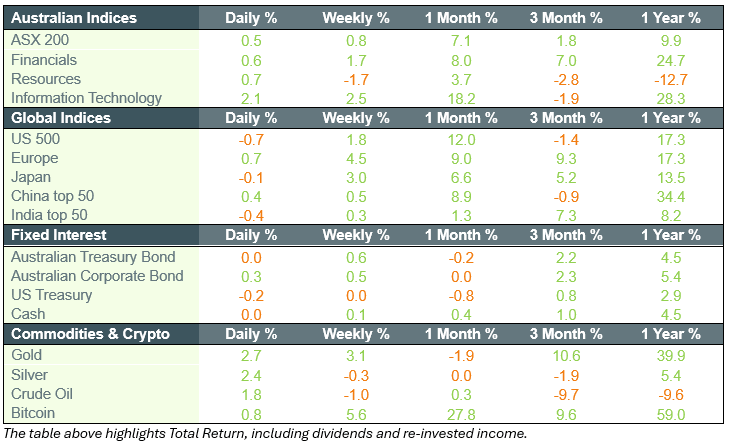

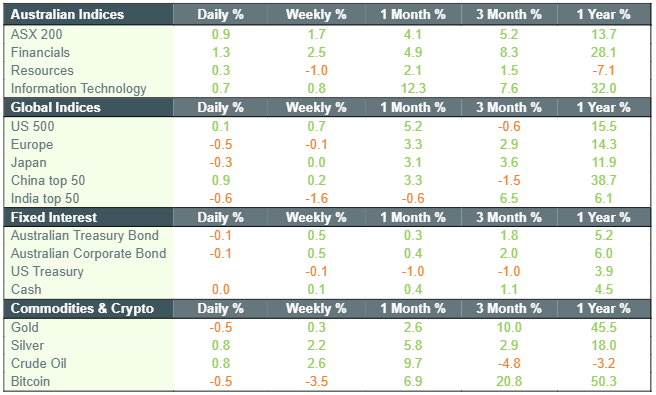

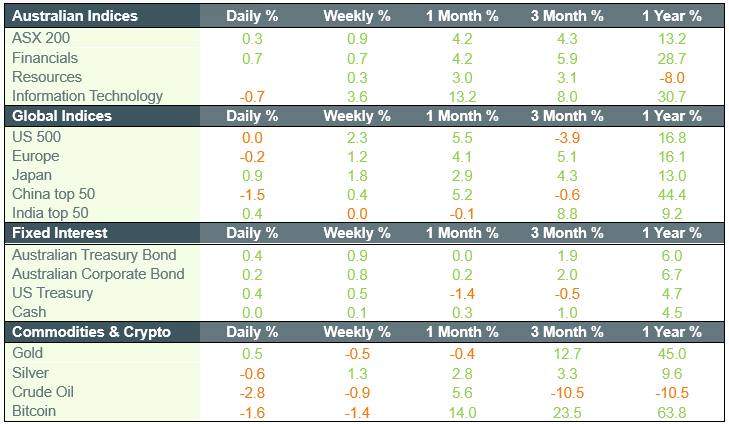

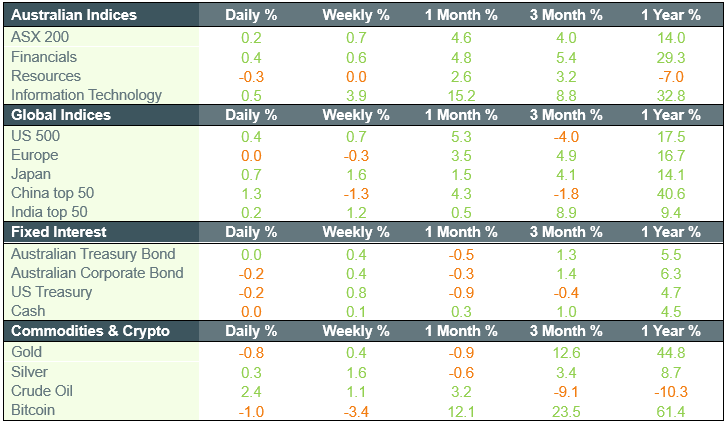

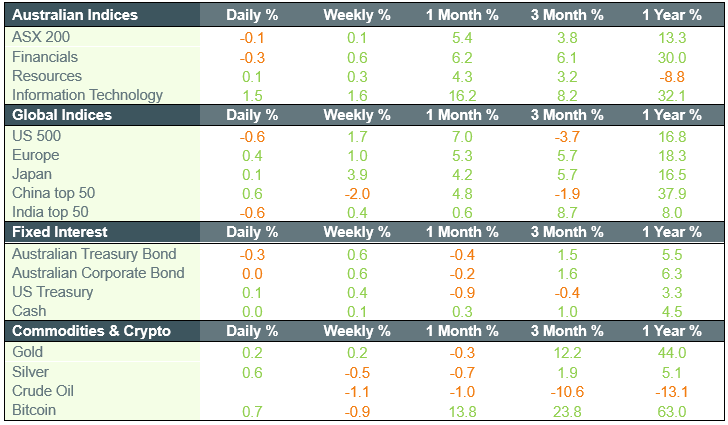

Market movements