Daily Market Update: 14 May, 2025

The key takeaways from the last 24 hours

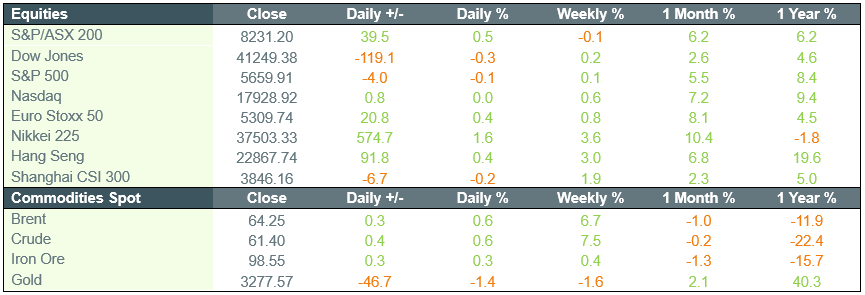

Tech surge sends ASX higher on US-China relations, gold miners reverse course as Genesis sinks

The local market followed the buoyant US lead higher, with the S&P/ASX200 (ASX:XJO) gaining 0.4 per cent. While a long way from the solid rally in the US, the energy and technology sectors were the biggest beneficiaries of cooling US-China trade relations, both rallying more than 3 per cent during the session. While their was little in the way of news, the likes of WiseTech (ASX:WST) added 4.9 per cent while Life360 (ASX:360) surged to an all-time high, gaining 14 per cent after reporting a far better than expected result. The group reported the addition of another 4.1 million users during the quarter, while also delivering a 32 per cent increase in revenue on the prior period. As with any rally, there are winners and losers, with gold miners bearing the brunt overnight. News that Citi had downgraded its expectations for the gold price, albeit only slightly, sent the likes of Genesis Minerals (ASX:GMD) and Capricorn Metals (ASX:CMM) down 10.7 and 9 per cent respectively.

Consumer staples weaken behind Coles (ASX:COL), Clarity reverses trend, Abacus Storage King Knock back bid

The short-term winners from global economic and trade upheaval were the losers on Tuesday, with both Woolworths (ASX:WOW) and Coles (ASX:COL) dropping more than 3 per cent each as traders shifted into the higher growth, trade-facing sectors during the session. Energy and mining stocks also benefitted behind BHP (ASX:BHP) and Woodside (ASX:WDS) which added 2.1 and 3.7 per cent respectively.

Shares in healthcare companies were buoyed by President Trump’s plans to cut US prescription drug prices, with Clarity Pharmaceuticals (ASX:CU6) adding 15 per cent during the session on hopes it may benefit. Biotech group PolyNovo (ASX:PNV) managed a near 15 per cent rally as the company confirmed its wound healing product NovoSorb could assist in treating type 1 diabetes after a human trial. Property owner Abacus Storage King (ASX:ASK) gained 1.7 per cent despite the group rejecting a proposal from an unexpected bidder to takeover the company.

US stocks hit highest point since February, recovering losses on chipmaker gains, Mag 7 outperform

The S&P500 led US markets higher overnight, with the index gaining 0.7 per cent while the Nasdaq jumped 1.6 per cent, as investors jumped back into market following news of the US-China trade deal. More importantly, though, was news that the Saudi government had plans to invest as much as US$1 trillion in the US amid a loosening of investment and export rules. The likes of NVIDIA (NYSE:NVDA) and Advanced Micro Devices (NYSE:AMD) surged by 5 and 4 per cent respectively, on news that both companies would supply Saudi Arabian firm Humain with chips for a massive data centre project.

In more positive news, inflation rose by less than expected for the month, as clothing and new car prices remain muted, causing President Trump to put more pressure on Jerome Powell to cut rates and weaken the dollar. More than 77 per cent of S&P500 companies that reported during the quarter, surprised positively according to data.