The key takeaways from the last 24 hours

Australian market hits new high

The Australian sharemarket extended its record-setting run, with the S&P/ASX 200 Index (ASX: XJO) rising 0.2 per cent to close at 8959.30, reaching its fifth all-time high in just over a week. A robust start to the earnings season helped fuel gains, with about half of reporting companies beating expectations, according to UBS. The market, however, showed signs of caution, as UBS noted that while upgrades slightly outpaced downgrades, the scale of revisions painted a less optimistic picture.

Banks lead while materials weigh

The banking sector provided a lift, with National Australia Bank Limited (ASX: NAB) jumping 2.7 per cent to $40.23 despite warning of higher operating expenses. Commonwealth Bank of Australia (ASX: CBA) rebounded 1.2 per cent to $170.19 following recent losses, while Westpac Banking Corporation (ASX: WBC) added 0.7 per cent and Australia and New Zealand Banking Group Limited (ASX: ANZ) slipped 1.5 per cent. On the downside, materials lagged due to weaker iron ore prices, dragging shares of BHP Group Limited (ASX: BHP), Rio Tinto Limited (ASX: RIO), and Fortescue Metals Group Limited (ASX: FMG) lower. BlueScope Steel Limited (ASX: BSL) fell 3.1 per cent after posting a sharp profit decline. Among movers, Lendlease Group (ASX: LLC) surged 6.7 per cent on a return to profitability, REA Group Limited (ASX: REA) rose 4.5 per cent on a CEO appointment, and DigiCo Infrastructure REIT (ASX: DGI) sank 14.1 per cent after slightly missing earnings expectations.

Global markets steady ahead of Fed

US markets remained near flat, with the S&P 500 Index (NYSE: SPX) and the Nasdaq Composite Index (NASDAQ: IXIC) showing little change, while the Dow Jones Industrial Average (NYSE: DJI) dipped 0.1 per cent. Attention has turned to upcoming earnings from major US retailers and Federal Reserve Chair Jerome Powell’s speech at Jackson Hole, which investors hope will offer clues on future rate cuts. Markets are anticipating a potential rate reduction in September, with the Fed’s July meeting minutes set for release midweek. In geopolitical developments, former President Donald Trump met with Ukraine’s President Zelensky and European leaders after talks with Russian President Putin, while Intel Corporation (NASDAQ: INTC) fell 3.7 per cent following news of potential White House involvement in the company.

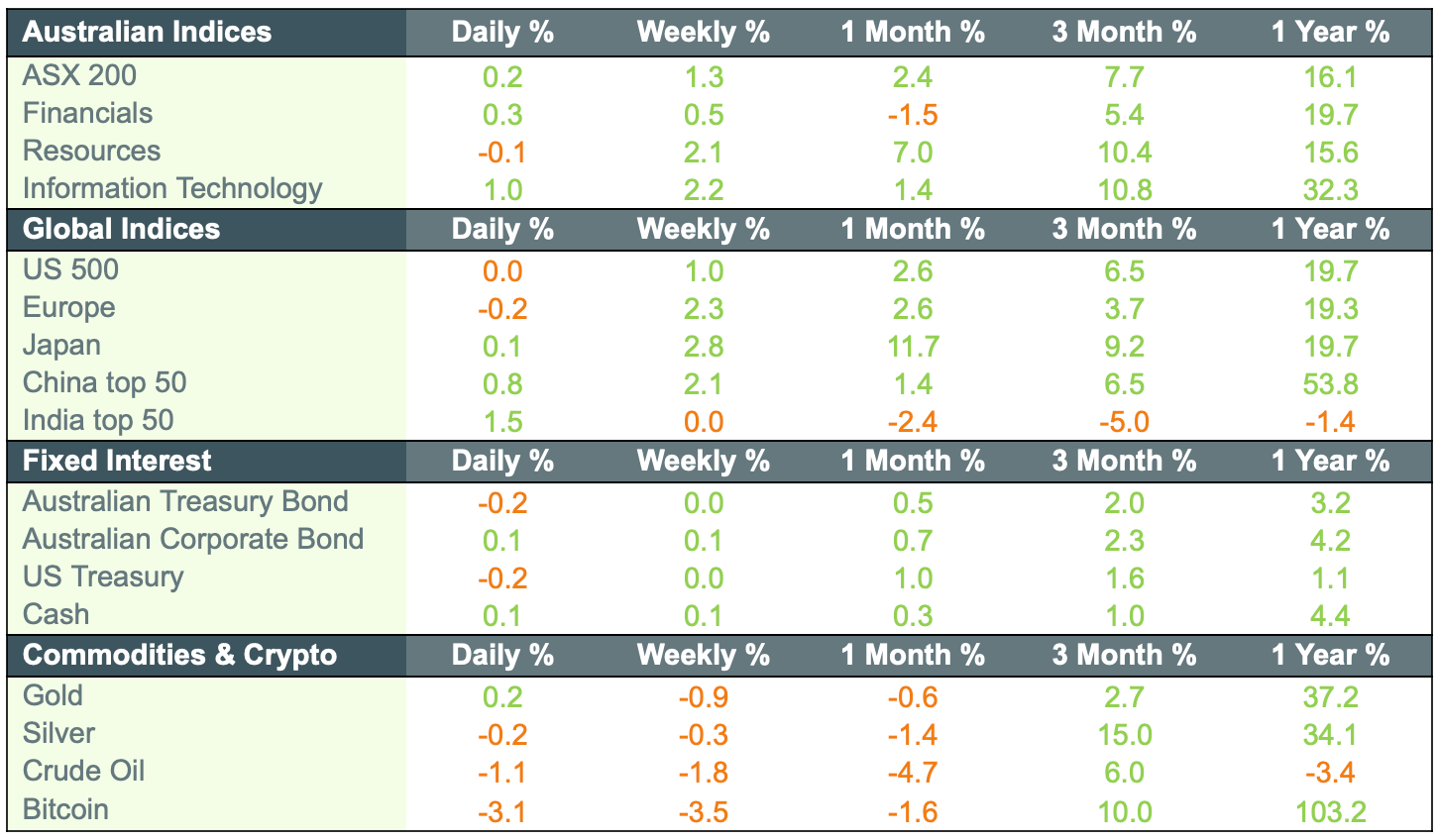

Market movements